What Moved the Market

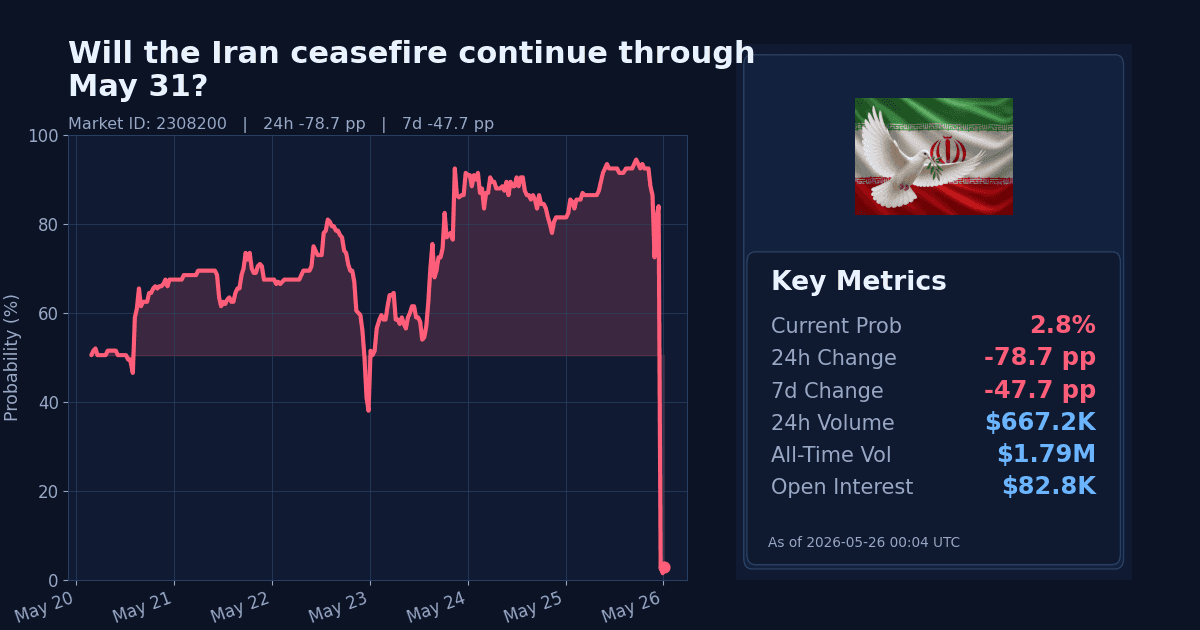

The Polymarket contract on whether the US–Iran ceasefire will continue through May 31 (ET) dropped sharply over the past day. As of May 26 (UTC), the implied probability is 2.8%, a 78.7 percentage-point decline over 24 hours.

This is an extreme single-day repricing by the market’s own historical yardstick (24h z-score: 320.0). The market opened on May 20 and covers outcomes through May 31 ET, with an additional day to allow for confirmation of any qualifying kinetic action under the resolution rules.

Why It Likely Moved

- The move appears driven by synchronized repricing in adjacent, shorter-dated markets: the May 25 and May 26 ceasefire contracts both collapsed in the past 24h (to 2.6% and 2.2%, respectively), aligning the curve around a potential late-May break rather than a steady continuation through month-end.

- Newsflow on May 25 characterized an emerging US–Iran deal as uncertain, with “significant disagreements” and lingering threats of renewed hostilities, which markets may have treated as a deterioration versus prior optimism (AP News; NPR).

- Additional political signaling tied potential Iran diplomacy to broader regional conditions, introducing linkage risk that could complicate timelines and enforcement, according to reporting on May 25 (AP News).

- The repricing also likely reflects proximity to the contract window end-date: with the month-end nearing, traders are more sensitive to any late-breaking developments that could trigger the market’s specific resolution condition (US-confirmed aerial kinetic action on Iranian soil) within the one-day confirmation window.

How Strong the Move Is

By the market’s own volatility measures, the 24-hour decline is extreme (24h z-score: 320.0), classifying this as a sharp, event-driven spike lower rather than routine noise. The 7-day change is -47.7 percentage points, while the weekly z-score reads as normal in context, indicating the magnitude is concentrated in this latest session.

Overall, this is a significant, abrupt repricing consistent with traders reacting to clustered signals and cross-contract alignment rather than a slow trend continuation.

Cross-Market Confirmation

- May 24 contract: 96.9% (24h: -2.15 pp). High odds for that earlier date diverge from the late-May markets, consistent with a potential inflection after May 24.

- May 25 contract: 2.6% (24h: -93.35 pp). Confirms the sharp late-May risk repricing.

- May 26 contract: 2.2% (24h: -89.75 pp). Confirms alignment with the main market’s move.

The term structure—strong May 24, weak May 25–26—supports the interpretation that traders are concentrating risk around the late-May window rather than a continuous, high-probability ceasefire through May 31.

News & Real-World Context

- On May 25, AP reported that Donald Trump linked any prospective Iran deal to additional countries joining the Abraham Accords, introducing broader conditions into the diplomacy framework (AP News).

- Also on May 25, AP described an emerging deal “to end the war” but noted unclear details on enforcement, timelines, and guarantees, underscoring uncertainty in the near term (AP News).

- NPR on May 25 reported signals of progress tempered by continued disagreements and the threat of renewed hostilities, conveying an unsettled backdrop rather than a finalized accord (NPR; NPR Up First).

Macro signals offer limited confirmation: WTI crude is at $90.9/bbl and fell 16.3% over the past week, the US Dollar Index edged up 0.27% over 7 days, and the VIX declined 6.9% over 7 days. These broader indicators point to easing risk premia rather than a systemic escalation impulse, suggesting the market move here is idiosyncratic relative to global macro pricing.

Bottom Line

Traders have marked down the probability that the US–Iran ceasefire remains in effect through May 31 to low single digits, with the curve pointing to elevated late-May risk. The move looks event-driven and concentrated in the latest session, supported by adjacent contracts and a news cycle emphasizing uncertainty in negotiations.

Absent corroborating broad risk signals, this appears to be a market-specific repricing tied to timing and resolution mechanics; further movement will likely depend on confirmations or denials of developments within the contract’s late-May window.

Market Conditions at Time of Writing

- Current Probability: 2.8%

- 24h Change: -78.7 pp

- 7d Change: -47.7 pp

- Volume (24h, $): 667,220.68

- Open Interest ($): 82,780.9

- Spread (pp): 0.8

- Z-score (24h): 320.0