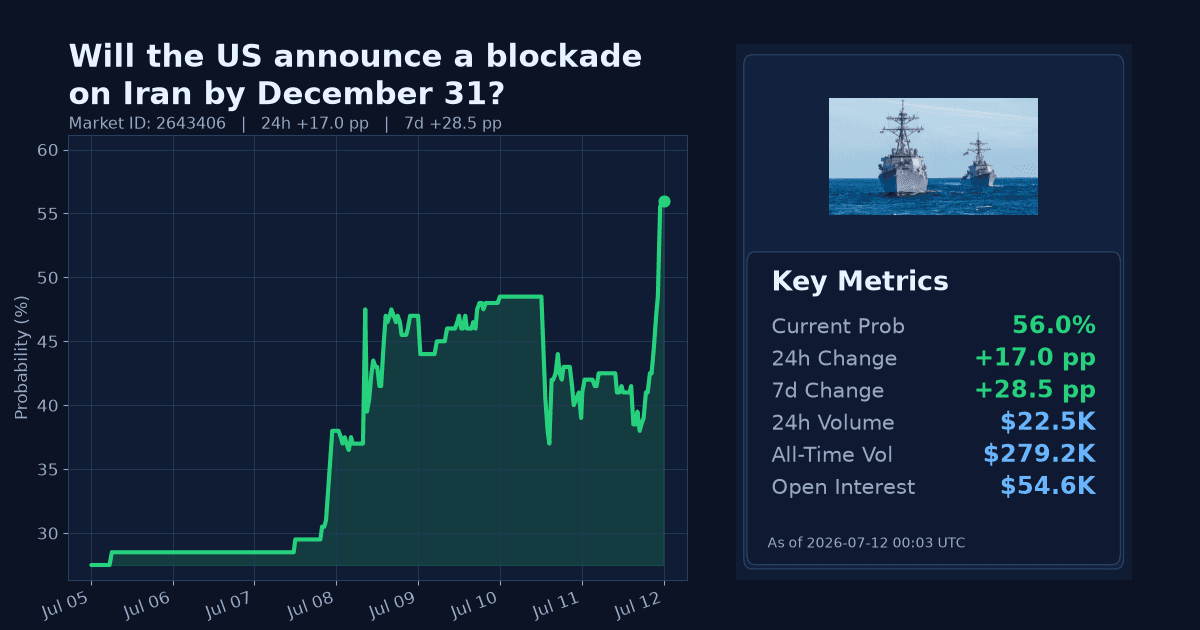

What Moved the Market

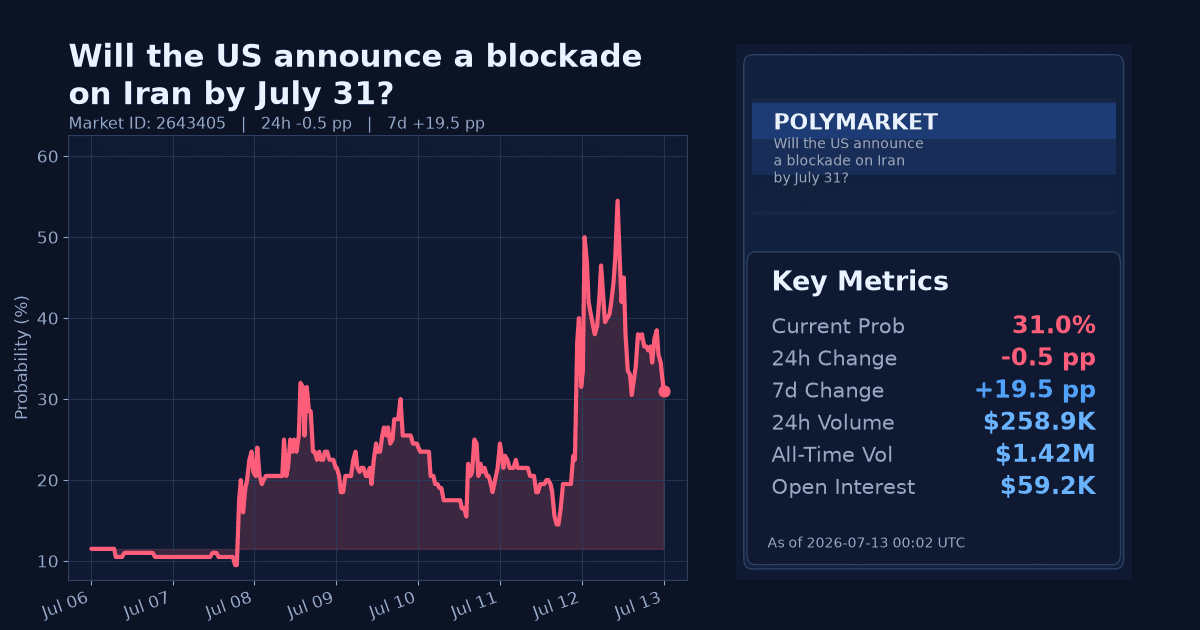

The Polymarket contract on whether the United States will announce a blockade on Iran by July 31, 2026 rose to 31% as of July 13. Over the past seven days, the market repriced higher by 19.5 percentage points. Within the last 24 hours, it edged down 0.5 percentage points.

The contract resolves "Yes" if, between June 22 and July 31, 2026, a U.S. official channel publicly announces a naval blockade involving Iran or traffic to/from Iranian ports or the Strait of Hormuz. The market remains sensitive to official signals and regional risk indicators given the short window to resolution.

Why It Likely Moved

- The repricing appears driven by increased diplomatic focus on Iran and the Gulf. The UK, in a July 10 statement at the UN Security Council, called for “de-escalation and a return to diplomacy,” underscoring elevated international attention to Iran-related tensions, according to the UK government.

- Markets reacted to Australian government messaging that highlighted instability risks and energy market impacts tied to the region. In a July 10 interview published by Australia’s Department of Foreign Affairs, Foreign Minister Penny Wong emphasized de-escalation and noted global energy market disruptions, with the discussion explicitly flagging the Strait of Hormuz (Australian government).

- The move aligns with energy-market signals: Brent crude rose 9.18% over the past week to $78.39/bbl, a pattern consistent with traders adding risk premia around potential shipping or supply disruptions in the Gulf (source: Yahoo Finance).

- The repricing follows a period where some official commentary suggested easing tensions and lower energy prices; however, subsequent price action indicates traders reassessed risk higher. On July 8, the Dutch central bank noted signs that “Iran and the US” were again finding a way forward and that energy prices were falling (De Nederlandsche Bank).

How Strong the Move Is

On a 7-day basis, the upward move is extreme by the market’s historical volatility (z-score ~8.34), indicating a sharp repricing toward higher odds within a short time window. This characterizes the weekly action as a significant spike rather than routine drift.

In the last 24 hours, the market ticked down 0.5 percentage points, but the intraday move registers as extreme by z-score (6.0). Given the small magnitude, this appears as an outsized statistical fluctuation against recent tight intraday ranges rather than a directional reversal.

Cross-Market Confirmation

- US-Iran Final Nuclear Deal by Aug 18, 2026 fell 11.0 pp over 7 days and 2.0 pp over 24 hours to 6.0%, reinforcing a shift away from near-term diplomacy and aligning with higher confrontation risk.

- Will the U.S. invade Iran before 2027? rose 6.0 pp over 7 days and 1.0 pp over 24 hours to 18.0%, a directional confirmation of rising geopolitical risk.

- Israel closes its airspace by July 15? is up 1.8 pp over 7 days and 0.35 pp over 24 hours to 4.0%, a modest move that weakly aligns with the broader risk tone.

News & Real-World Context

- On July 10, the UK told the UN Security Council it “stands with partners in calling for de-escalation and a return to diplomacy,” framing the Iran file in multilateral terms and signaling a desire to reduce tensions, per the UK government.

- Also on July 10, Australia’s Foreign Minister Penny Wong, in an official interview, stressed the need for de-escalation and cited disruptions to global energy markets, with the discussion highlighting the Strait of Hormuz as a focal point (Australian government).

- On July 8, the Dutch central bank observed that Iran–US dynamics appeared to be improving and that energy prices were declining, though subsequent market data show Brent rising week-on-week (De Nederlandsche Bank).

Bottom Line

Traders sharply increased the probability of a U.S. blockade announcement within the July 31 window, consistent with higher perceived Gulf risk and a concurrent rise in oil prices. Official statements are emphasizing de-escalation, creating a tension between diplomatic intent and risk premia in markets.

Given the extreme 7-day move and confirming signals in related contracts, the repricing looks like a near-term risk spike rather than a durable structural shift.

Market Conditions at Time of Writing

- Current Probability (%): 31.0

- 24h Change (pp): -0.5

- 7d Change (pp): 19.5

- Volume (24h, $): 258,908.92

- Open Interest ($): 59,206.07

- Spread (pp): 1.0

- Z-score (24h): 6.0