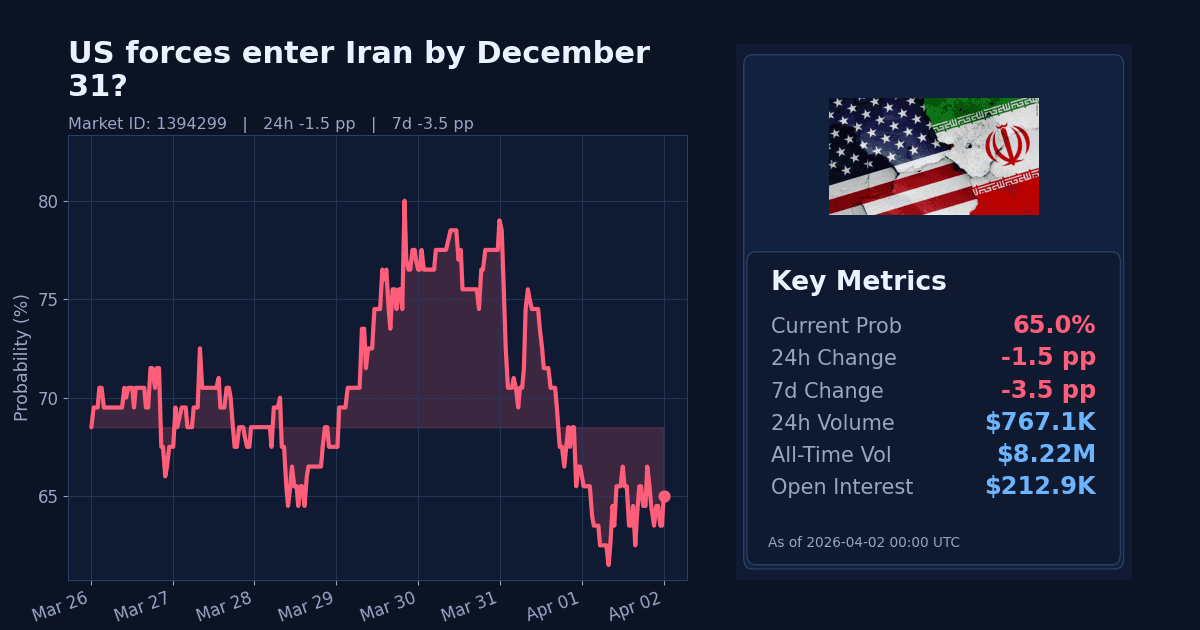

What Moved the Market

The Polymarket contract “US forces enter Iran by December 31?”—which requires active U.S. military personnel to physically enter Iran’s terrestrial territory before 2026‑12‑31—fell about 1.5 percentage points over the past 24 hours to 65%.

Over the last 7 days, pricing is down roughly 3.5 percentage points. Despite the modest point moves, the platform’s z‑score flags the 24‑hour shift as “extreme,” relative to recent trading patterns.

Why It Likely Moved

- The repricing appears driven by official U.S. messaging that operational objectives are close to being met and the campaign timeline is “weeks, not months,” according to an interview published by the U.S. State Department (Apr 1, 2026). The emphasis on achieving goals without signaling a ground incursion may have reduced odds on a physical entry into Iran.

- Markets reacted to signs of de‑escalation: global equities rose and oil eased intraday on renewed hopes the Iran war could be winding down, per AP News (Apr 1, 2026).

- The pullback also coincided with anticipation around a national address on Iran by President Trump, highlighted by AP News (Apr 1, 2026), which could clarify strategy and reduce uncertainty about escalation pathways.

- U.S. operational updates stressed tempo and efficiency of ongoing strikes (air/naval/missile suppression) rather than ground maneuver, as noted by the Department of War’s coverage of CENTCOM and Operation Epic Fury, see war.gov (Mar 31, 2026). This likely reinforced the market’s focus on the contract’s strict requirement for terrestrial entry.

- Macro corroboration is mixed: while AP reported oil softening on de‑escalation hopes, WTI still sits near $98.86/bbl and is up about 9.46% over 7 days and 38.79% over 30 days, indicating broader energy risk remains elevated (source: Yahoo Finance).

How Strong the Move Is

The 24‑hour decline of ~1.5pp registers an “extreme” z‑score (12.0), suggesting an outsized shift versus this market’s recent intraday volatility. The 7‑day move of ~3.5pp lower shows a “sharp” downside trend on a weekly basis.

In classification terms, this looks like a downside spike that continues a short, week‑long drift lower rather than a full reversal of the broader thesis.

Cross-Market Confirmation

- “US forces enter Iran by April 30?” is priced at 53%. With no 24h/7d delta published, contemporaneous confirmation is unclear; the elevated near‑term level does not fully validate today’s softening in the year‑end market.

- “Trump announces end of military operations against Iran by April 7th?” stands at 12% (no deltas available), and “by April 15th?” at 26% (no deltas available). These levels suggest low odds of an immediate end to operations, a signal that diverges from any notion of rapid de‑escalation and leaves near‑term escalation risk unresolved.

News & Real-World Context

- The U.S. State Department published an interview on April 1 in which Secretary of State Marco Rubio outlined four objectives—degrading Iran’s air force, navy, missile launchers, and defense industrial base—and said the campaign is on or ahead of schedule and measured in “weeks, not months” (U.S. State Department, Apr 1, 2026).

- The Department of War highlighted CENTCOM performance and “wartime speed” in Operation Epic Fury, reinforcing the current mode of operations (war.gov, Mar 31, 2026).

- AP reported global shares higher and oil lower on April 1 as investors bet on prospects of the Iran war ending, signaling risk‑premium compression in energy and broader assets (AP News, Apr 1, 2026).

- AP also flagged a forthcoming national address by President Trump on Iran, a potential catalyst for policy clarity (AP News, Apr 1, 2026).

- The UK government announced additional air‑defense support for Gulf partners during a Middle East visit, underscoring regional defense posture rather than ground operations in Iran (UK Government, Mar 31, 2026).

Bottom Line

Pricing for a U.S. terrestrial entry into Iran by December 31 edged lower, with an outsized 24‑hour z‑score, likely on official U.S. timelines suggesting objectives are near and broader signals of potential de‑escalation. Cross‑market levels remain mixed, keeping near‑term risk elevated even as the year‑end contract softened.

This looks like a short‑term repricing pending presidential guidance and further government signals, not yet a structural shift in the thesis.

Market Conditions at Time of Writing

- Current Probability: 65%

- 24h Change: -1.5pp

- 7d Change: -3.5pp

- Volume (24h, $): 767,069.76

- Open Interest ($): 212,911.72

- Spread (pp): 1.0

- Z-score (24h): 12.0