What Moved the Market

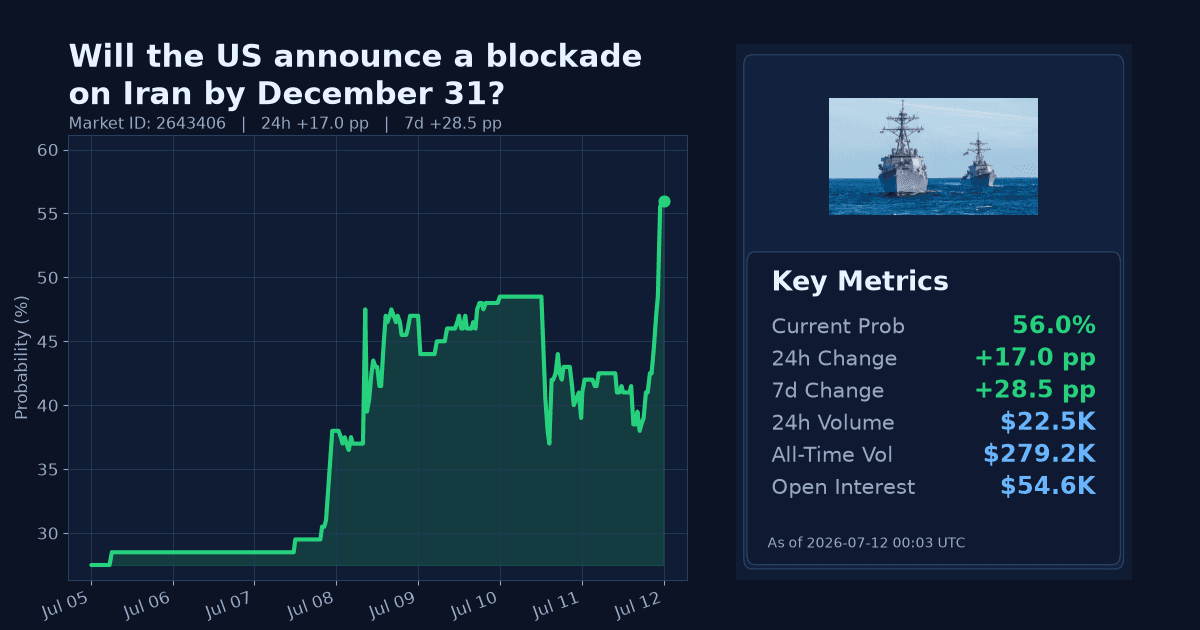

Polymarket traders sharply repriced the contract “Will the US announce a blockade on Iran by December 31?” The probability rose 17 percentage points in 24 hours to 56%, and is up 28.5pp over the past week. The market covers announcements made between June 22, 2026 (creation) and 11:59 PM ET on December 31, 2026.

This is an extreme, upward move by the platform’s own z-score metrics, indicating an unusual shift versus recent trading history rather than routine noise.

Why It Likely Moved

- Markets reacted to new public threats directed at Iran, including posts and statements highlighted on July 11 that referenced the Strait of Hormuz and escalatory rhetoric toward Tehran, as reported by NPR and AP News.

- The repricing follows heightened official attention to Iran and de-escalation at the UN: on July 10, the UK government called at the UN Security Council for de-escalation and a return to diplomacy on Iran, signaling active allied engagement on the issue.

- On July 10, Australia’s Foreign Minister underscored risks around Hormuz and energy markets, while pressing for de-escalation and diplomacy, according to the Australian government. This official framing reinforces market focus on maritime security.

- European institutional attention also rose: on July 8, a European Parliament written question pressed the Commission on possible EU complicity in a US war of aggression against Iran, indicating political scrutiny of conflict dynamics.

- Energy markets showed a modest risk bid over the week: WTI crude rose about 4% over 7 days to $71.41/bbl as of July 10, per Yahoo Finance data, consistent with traders pricing greater shipping and MENA disruption risk amid Iran tensions.

How Strong the Move Is

The 24-hour change (+17pp) and 7-day change (+28.5pp) are both characterized as extreme by platform z-scores (24h z≈60; 7d z≈110). This qualifies as an extreme spike rather than normal variance.

Given the sustained 7-day climb, the move looks like a fast, week-long repricing rather than a single print anomaly. Still, the extremity of the z-scores suggests elevated short-term momentum sensitivity to headlines.

Cross-Market Confirmation

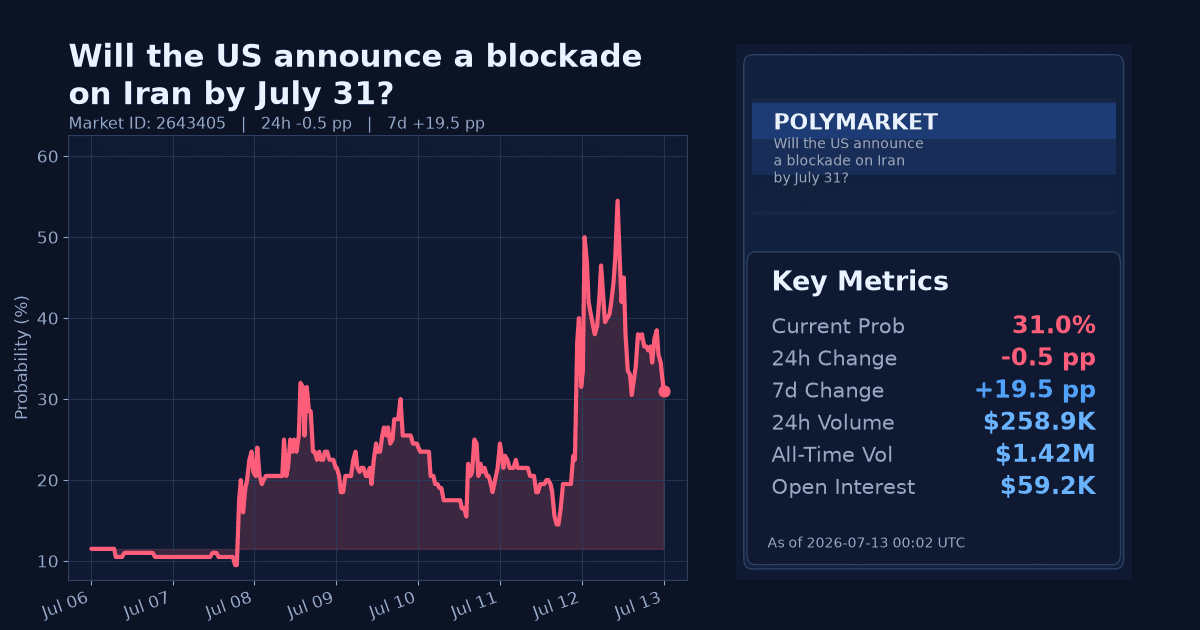

- The shorter-dated “by July 31” blockade market rose to 31% (delta_24h +7.0pp; delta_7d +19.0pp), aligning directionally with the main contract’s surge.

- The “by August 31” market increased to 42% (delta_24h +10.5pp), reinforcing earlier-timeline escalation risk.

- A related Hormuz security market — “Iran commits not to attack ships in Hormuz by Sunday?” — fell to 2.4% (delta_24h −14.3pp), consistent with reduced confidence in near-term de-escalatory commitments.

Overall, related markets corroborate the upward move in blockade-announcement risk, particularly over nearer horizons.

News & Real-World Context

On July 11, reporting described new threats by Donald Trump toward Iran following chants at Ayatollah Ali Khamenei’s funeral and US calls tied to keeping the Strait of Hormuz open, elevating tensions around navigation and enforcement signals, per NPR and AP News. Separately, AP noted on July 11 that Trump suggested a “standing order” to attack Iran in a specific contingency, underscoring the escalatory tone in public rhetoric (AP News).

Government signals emphasized diplomacy and maritime stability. On July 10, the UK government told the UN Security Council it stands with partners in calling for de-escalation and a return to diplomacy on Iran. The same day, Australia’s Foreign Minister, in an official interview transcript (July 10), highlighted Brink-of-war concerns, the Strait of Hormuz, and energy-market impacts while calling for stability and negotiations. At the EU level, a July 8 European Parliament written question pressed the Commission on whether the EU is complicit in a US war of aggression against Iran, reflecting institutional scrutiny of the conflict context.

Bottom Line

An extreme, headline-driven repricing pushed the December 31 blockade-announcement odds into the mid-50s. Public threats and concentrated official attention on Iran and Hormuz appear to have raised perceived near- to medium-term escalation risk.

Given the contract window through year-end, this looks like a sharp, event-driven adjustment that could persist if rhetoric and official focus remain elevated, but its durability is uncertain and likely headline-sensitive.

Market Conditions at Time of Writing

- Current Probability: 56.0%

- 24h Change: +17.0pp

- 7d Change: +28.5pp

- Volume (24h, $): 22472.7

- Open Interest ($): 54623.71

- Spread (pp): 4.0

- Z-score (24h): 60.0