What Moved the Market

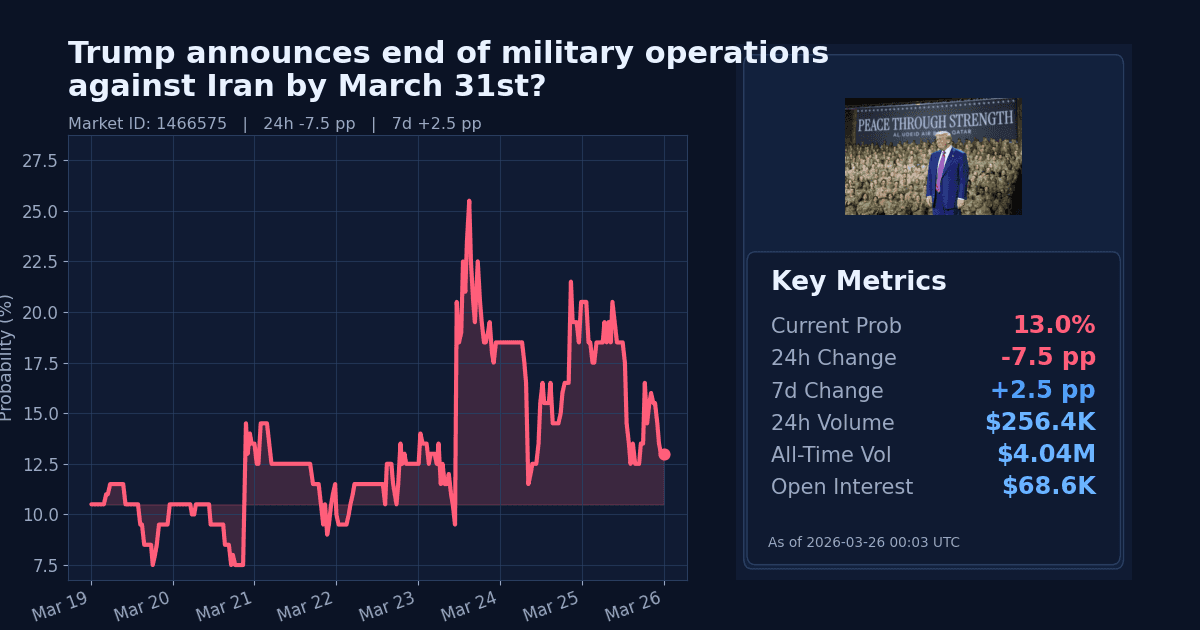

The Polymarket contract on whether President Trump will announce the end of U.S. military operations against Iran by March 31, 2026 moved down sharply over the last 24 hours. The probability fell 7.5 percentage points to 13% as of March 26, 2026.

This contract covers a narrow window: operations initiated on February 28, 2026, and the market resolves based on a clear, public announcement by March 31 (ET). No qualifying official statement has been cited in the market’s tracked context to date.

Why It Likely Moved

- Repricing appears driven by analysis indicating the U.S. air campaign remains active, with a sustained tempo of hundreds of targets struck per day, signaling operations are ongoing rather than concluded.

- Markets reacted to reports that the Pentagon ordered additional 82nd Airborne troops to the Middle East, which reduced the perceived likelihood of an imminent declaration that operations have ended.

- The move follows the absence of any qualifying U.S. government or presidential announcement, with the contract’s deadline now days away, increasing the weight of “no news” in pricing.

- Cross-market signals show low odds of a ceasefire by March 31 but materially higher odds by April 30, pointing to a timeline shift rather than immediate de-escalation.

- Energy benchmarks remain elevated on a 30‑day view despite a weekly pullback (WTI near $91, Brent near $98), consistent with ongoing conflict risk rather than a declared conclusion this month.

How Strong the Move Is

The 24-hour decline of 7.5 percentage points to 13% registers as an extreme down move by the market’s own z‑score (24h z=32.0), indicating a sharp repricing relative to recent trading history. This qualifies as a significant, discrete downtick rather than routine noise.

Over seven days, however, the contract is up 2.5 percentage points, and the 7‑day z‑score reads as normal and flat. Taken together, the latest action looks like a sharp 24‑hour adjustment within an otherwise range‑bound weekly profile, not yet a multi‑day trend reversal.

Cross-Market Confirmation

- “US x Iran ceasefire by March 31?” at 14% aligns with this market’s low odds, confirming weak expectations for an immediate halt.

- “US x Iran ceasefire by April 30?” at 49% diverges on timing, suggesting markets see a higher chance of cessation next month rather than by March 31.

- “US forces enter Iran by March 31?” at 19% indicates non‑trivial escalation risk still being priced, consistent with skepticism about an imminent end-of-operations announcement.

News & Real-World Context

- Independent analysis describes the U.S. strike campaign as having settled into a sustainable pace (roughly 300–500 targets per day after the initial surge), implying continued operations rather than termination.

- NPR reported the Pentagon ordered additional 82nd Airborne Division troops to deploy to the Middle East, emphasizing ongoing military posture and options.

- An AP-NORC poll found most Americans view U.S. action against Iran as having gone too far, underscoring domestic political pressures while not indicating any official conclusion of operations.

- Amnesty International criticized threats regarding strikes on power infrastructure, and reporting on Trump’s rescheduled China trip to May cited the Iran war as the reason for earlier delays—both signals describe an active, unresolved conflict.

- Energy markets reflect the backdrop: WTI around $90.96 and Brent around $97.83 are down over the week (about 6–9%) but up roughly 37% over 30 days, consistent with a persistent conflict premium despite short‑term easing.

Bottom Line

Pricing dropped sharply as traders marked down the odds of an official “end of operations” announcement before the March 31 deadline amid continuing strike activity and fresh deployments. The move looks like a near‑term repricing rather than a durable multi‑week trend. With only days left in the window and no qualifying statements, near‑term resolution risk skews toward “No” unless an explicit announcement arrives.

Market Conditions at Time of Writing

- Current Probability (%): 13.0

- 24h Change (pp): -7.5

- 7d Change (pp): 2.5

- Volume (24h, $): 256,360.24

- Open Interest ($): 68,636.57

- Spread (pp): 2.0

- Z-score (24h): 32.0