What Moved the Market

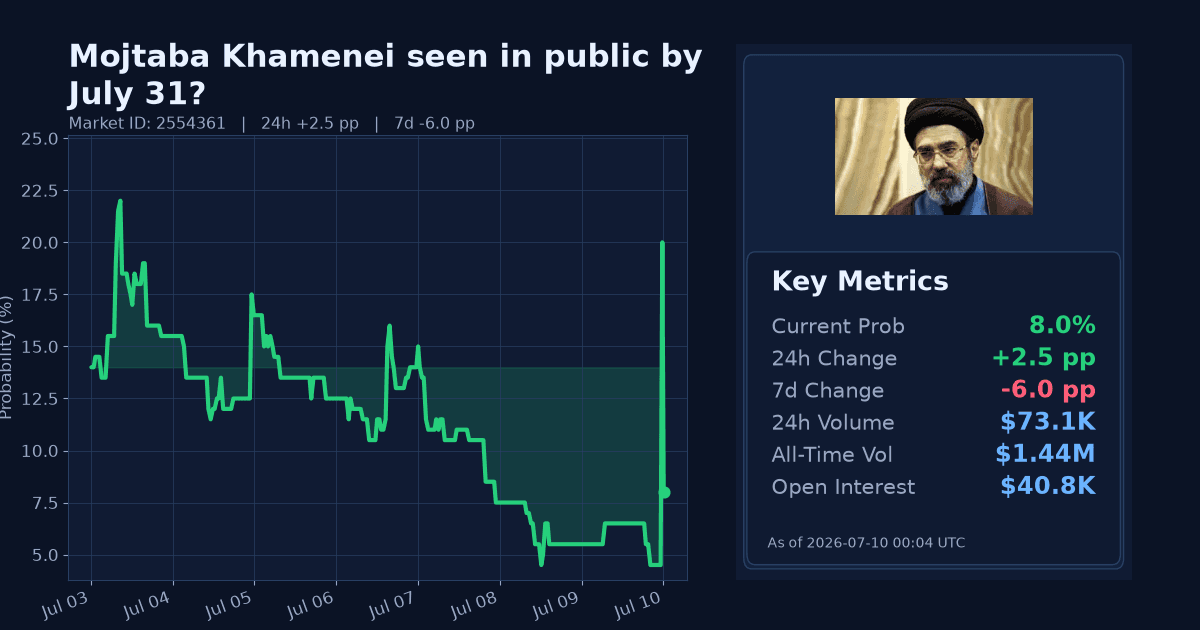

The Polymarket contract "Mojtaba Khamenei seen in public by July 31?" rebounded to 8.0% as of July 10. That is a 2.5 percentage-point increase over the past 24 hours, reversing part of a week-long decline.

Over seven days, the contract remains down 6.0 percentage points, indicating the latest uptick follows a broader pullback since early July. The market window runs from June 15, 2026 through July 31, 2026 (ET).

Why It Likely Moved

- The 24h repricing appears driven by renewed official attention on Iran, including the UK Foreign, Commonwealth and Development Office summoning Iran’s Chargé d’Affaires on July 7, as stated by the UK government.

- The move also comes alongside European Parliament activity that keeps Iran-linked issues salient: a July 8 written question on potential EU complicity in the US war against Iran and a July 9 question on external interference, both recorded by the European Parliament and here.

- Broader conflict context remains in the discourse, with a July 9 analysis by CSIS referencing the US–Israel war with Iran and associated regional disruptions, which can increase the likelihood of verifiable media coverage from Iran-related actors.

- Macro signals show energy markets attentive to Iran risk: Brent crude stands at $76.1/bbl, up ~6% week-over-week but down ~17% month-over-month, indicating shifting risk premia that markets may be monitoring alongside Iran developments.

How Strong the Move Is

On a 24-hour basis, the z-score is 8.0, flagged as an “extreme” upward move relative to recent trading. This suggests a sharp, statistically unusual bounce.

Over seven days, the market shows an “extreme” downward move (z-score 26.0), classifying the current rise as a short-term spike within a broader downtrend rather than a clear reversal.

Cross-Market Confirmation

- Near-dated analog: "Mojtaba Khamenei seen in public by July 15?" is at 4.9% (delta_24h +0.95pp; delta_7d -7.6pp). This modest 24h rise confirms the short-term bounce, while the 7d decline aligns with the broader downtrend.

- Regime-change proxy: "Reza Pahlavi head of state in Iran end of 2026?" at 5.0% (delta_24h +1.85pp; delta_7d +2.0pp) shows a mild uptick that only partially aligns and may reflect a different theme.

- Escalation risk: "US announces a blockade on Iran by July 31?" at 24.0% (delta_24h +3.0pp; delta_7d +12.0pp) has risen more strongly, a divergent signal that does not clearly validate the appearance thesis.

News & Real-World Context

- On July 7, the UK government (FCDO) summoned Iran’s Chargé d’Affaires in London following a UK court case tied to an attack on an Iran International journalist, underscoring official scrutiny of Iran-related activities.

- The European Parliament recorded a July 8 written question on whether the EU is complicit in the US war against Iran (EP link) and a July 9 question on external interference of Islamic fundamentalism in Europe (EP link), signaling continued institutional attention to Iran-linked security and foreign policy issues.

- A July 9 CSIS analysis highlights ongoing conflict dynamics involving Iran and their spillover into regional events and investor sentiment.

- Separately, the Dutch central bank noted on July 8 that the US and Iran “seem” to be engaging again, with energy price relief for consumers, in a DNB blog. This contrasts with some escalation signals and may help explain conflicting cross-asset cues. Brent crude is $76.1/bbl (+~6% w/w, −~17% m/m).

Bottom Line

The contract’s price has snapped higher on an extreme 24h basis but remains well below earlier levels after an extreme 7d decline. Official UK and EU actions keep Iran in the spotlight, which may support near-term interest, but cross-market and macro signals are mixed.

Overall, this looks like a short-term bounce within a broader downtrend rather than a clear structural shift.

Market Conditions at Time of Writing

- Current Probability: 8.0%

- 24h Change: +2.5pp

- 7d Change: −6.0pp

- Volume (24h): $73,146.75

- Open Interest: $40,798.10

- Spread: 1.0pp

- Z-score (24h): 8.0