What Moved the Market

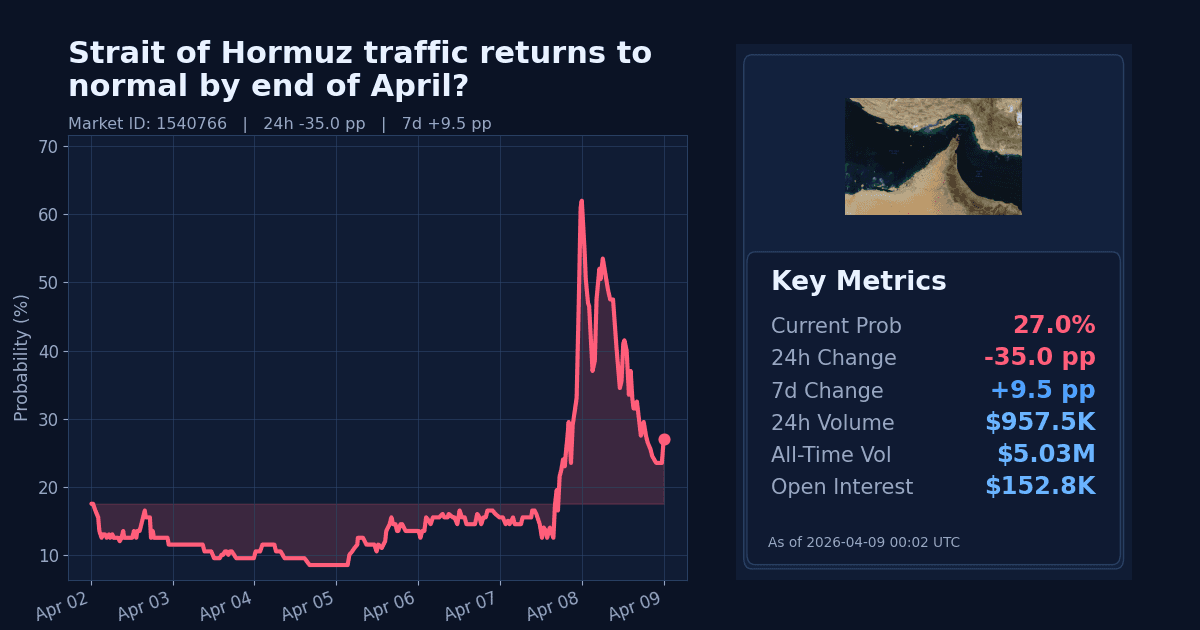

The Polymarket contract on whether Strait of Hormuz traffic returns to “normal” (IMF Portwatch 7‑day moving average of transit calls ≥60 on any date between March 9 and April 30, 2026) sold off sharply. As of April 9, the implied probability is 27%, down 35 percentage points over 24 hours.

This marks a sharp reversal from earlier in the week; the market is still up 9.5 points over seven days, but the latest session erased most of the recent rally.

Why It Likely Moved

- Repricing appears driven by continued operational caution from carriers, with an industry group saying Norwegian ships are not yet ready to resume Hormuz transits due to security concerns (Reuters via Ground News, April 8).

- Markets reacted to policy uncertainty after reports that Iran proposed collecting tolls on vessels transiting Hormuz, which legal experts say would violate trade norms and maritime law (AP News, April 8).

- The repricing follows mixed signals: French President Emmanuel Macron said more than 15 countries plan to facilitate access to the strait (Ground News, April 8), but implementation timelines are unclear.

- Official statements acknowledge a ceasefire, but do not resolve maritime specifics: the UK government (Foreign Secretary statement, April 8) noted a ceasefire involving the US, Israel and Iran; simultaneously, the UK expressed regret over a failed UN resolution on the Middle East at the Security Council on April 7 (UK government), underscoring contested diplomacy.

- Time compression may be contributing: fewer than three weeks remain for the 7‑day moving average to reach ≥60 before April 30, requiring sustained flows rather than a one‑off uptick.

How Strong the Move Is

The 24‑hour decline (−35pp) is classified as extreme by the market’s own z‑score framework, indicating an outsized session relative to recent trading. This points to a sharp downside shock rather than routine noise.

Over seven days, the market is still up (+9.5pp) with an extreme 7‑day z‑score, suggesting volatility has been elevated and the latest move constitutes a reversal from an earlier upswing.

Cross-Market Confirmation

- US × Iran ceasefire by April 7 is priced at 99.5% (Δ24h +0.65pp; Δ7d +90.95pp), confirming de‑escalation expectations elsewhere while diverging from the drop in Hormuz normalization odds.

- “Will Iran strike UAE again in March?” sits at 99.9% (Δ24h −0.05pp; Δ7d +24.2pp). Limited day‑over‑day movement; legacy risk pricing offers little confirmation for near‑term traffic normalization.

- “Will the Iranian regime fall by April 30?” remains low at 3.1% (Δ7d −0.75pp), indicating macro‑political regime risk is not the driver; this also diverges from the operational concerns reflected in shipping.

News & Real-World Context

Reports on April 8 indicated carriers remain cautious: Norwegian ships are not ready to resume transits through Hormuz pending clearer protections (Reuters via Ground News). The same day, AP News reported Iran’s proposal to collect tolls in the strait, which international legal experts say would contravene maritime norms, adding uncertainty over costs and legality.

Official signals are mixed. The UK government (April 8) acknowledged a ceasefire involving the US, Israel and Iran, while on April 7 the UK explained its vote at the UN Security Council following a failed Middle East resolution (UK government). On April 8, the European Parliament registered a written question highlighting navigation‑rights issues in Hormuz (European Parliament), emphasizing ongoing legal sensitivities around the waterway.

Broader commentary underscores uncertainty: Axios noted that even with a reported ceasefire, large‑scale resumption of oil shipping is not guaranteed due to insurer and carrier caution, and AP News detailed that a tentative two‑week truce took effect with explicit limits. Separately, AP News reported divergent interpretations of the ceasefire, adding to implementation uncertainty.

Macro context: Brent crude is at $97.1/bbl, down about 4.0% over seven days (as of April 8), which is consistent with some easing in risk premia but does not, by itself, confirm on‑the‑water normalization.

Bottom Line

Traders sharply cut the odds that IMF Portwatch will show “normal” Hormuz traffic by April 30, reflecting persistent operational and legal uncertainty despite formal ceasefire signals and facilitation plans. With the contract window closing and the threshold defined by a 7‑day average, the market appears to be demanding clear and sustained evidence in Portwatch data.

This looks like a short‑term, time‑sensitive repricing rather than a structural shift, pending observable transit recovery.

Market Conditions at Time of Writing

- Current Probability: 27%

- 24h Change: −35pp

- 7d Change: +9.5pp

- Volume (24h): $957,538.97

- Open Interest: $152,754.52

- Spread: 1pp

- Z-score (24h): 140.0 (extreme)