What Moved the Market

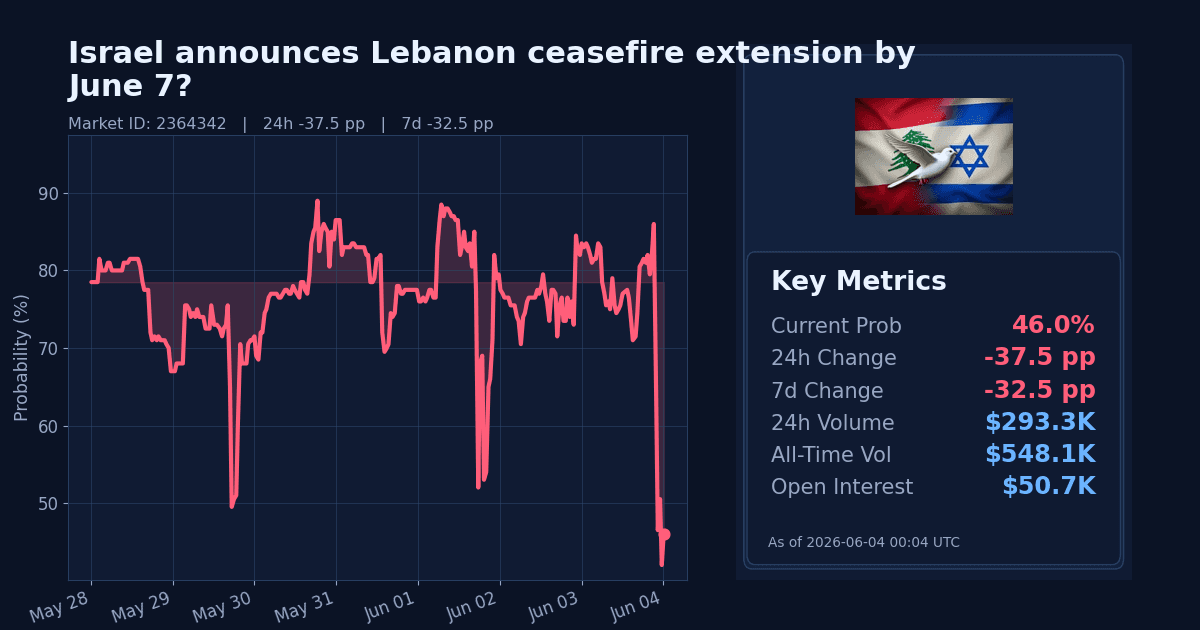

The Polymarket contract on whether Israel will announce an extension of the Lebanon (Hezbollah) ceasefire by June 7 dropped sharply over the last day. As of June 4 (UTC), implied probability stands at 46%, down 37.5 percentage points over 24 hours.

The market, which resolves on an official Israeli announcement extending the April 16 ceasefire (including any new agreement) by 11:59 PM IDT on June 7, has also fallen 32.5pp over the past week, indicating a sustained repricing into the contract deadline.

Why It Likely Moved

- The repricing appears driven by reports of Israeli strikes just south of Beirut, including near Tyre and Khaldeh, ahead of a second day of ceasefire talks on June 3, heightening tensions and casting doubt on near-term extensions, according to AP News (June 3).

- Markets reacted to an official warning by the UK at the UN Security Council that escalation in Lebanon and across the Blue Line “risks undermining critical negotiations to achieve peace across the region,” as stated by the UK government (June 1).

- The repricing follows increased U.S. congressional scrutiny of regional escalation risks, with the U.S. House taking up — and, according to NPR, passing — a war powers resolution aimed at ending hostilities with Iran on June 3; while not Lebanon-specific, it adds to a backdrop of contested escalation management.

- Into the deadline, traders may be demanding higher conviction for a qualifying Israeli announcement, given the contract’s strict requirement for clear, public confirmation from the Israeli government.

How Strong the Move Is

This is an extreme, directionally large decline over 24 hours: down 37.5pp to 46%. The platform’s 24h z-score flag marks the move as “extreme” relative to the market’s recent trading history. The 7-day slide of 32.5pp reinforces that this is not a one-off print.

With both 24h and 7d z-scores flagged as extreme, the move classifies as a sharp, deadline-proximate selloff rather than routine noise. Intraday, a +12.5pp uptick over the last hour highlights elevated volatility but does not alter the broader downtrend.

Cross-Market Confirmation

- Israel × Iran permanent peace deal by June 30, 2026 is at 6.6% (−0.35pp 24h; −12.6pp 7d). The 7d decline aligns with weaker expectations for regional de-escalation, consistent with the main market’s selloff.

- US announces new Iran agreement/ceasefire extension by June 7 sits at 11.0% (+1.0pp 24h; −34.0pp 7d). The week-long drop corroborates lower odds of near-term agreements; the slight 24h uptick diverges marginally.

- US × Iran permanent peace deal by June 30, 2026 is at 25.0% (+2.0pp 24h; −20.0pp 7d). The 7d decline supports the broader de-risking thesis; the 24h gain is a short-term divergence.

Overall, related markets mostly confirm a 7-day shift toward reduced odds of rapid diplomatic breakthroughs, even if 24h prints are mixed.

News & Real-World Context

- On June 3, Israeli strikes hit areas just south of Beirut, including near Tyre and Khaldeh, as a second day of ceasefire talks was set to proceed, per AP News. This development raised near-term tension around the Lebanon front.

- On June 1, the UK’s Chargé d’Affaires to the UN warned the Security Council that escalating violence across the Blue Line threatens to undermine negotiations, according to the UK government. As an official government statement, this is a primary policy signal on diplomatic risk.

- U.S. lawmakers again considered constraints on the use of force against Iran, reflecting ongoing debate over escalation management; the House passed a war powers measure on June 3, as reported by NPR and covered in parallel by AP News (June 3).

- Macro backdrop: Brent crude is at $97.14/bbl, up roughly 3% over the past week, suggesting a modest energy risk premium persists amid regional tensions (Yahoo Finance, June 3).

Bottom Line

Pricing for an Israeli announcement to extend the Lebanon ceasefire by June 7 has fallen sharply, with both 24h and 7d moves flagged as extreme. The drop aligns with reported Israeli strikes near Beirut and the UK’s UN warning that Blue Line escalation is jeopardizing negotiations.

Absent clear, public confirmation from the Israeli government, markets are discounting a near-term extension. The move looks deadline-driven and event-specific rather than structural, but volatility remains elevated.

Market Conditions at Time of Writing

- Current Probability: 46%

- 24h Change: -37.5pp

- 7d Change: -32.5pp

- Volume (24h): $293,296.75

- Open Interest: $50,691.56

- Spread: 1.0pp

- Z-score (24h): 122.0