What Moved the Market

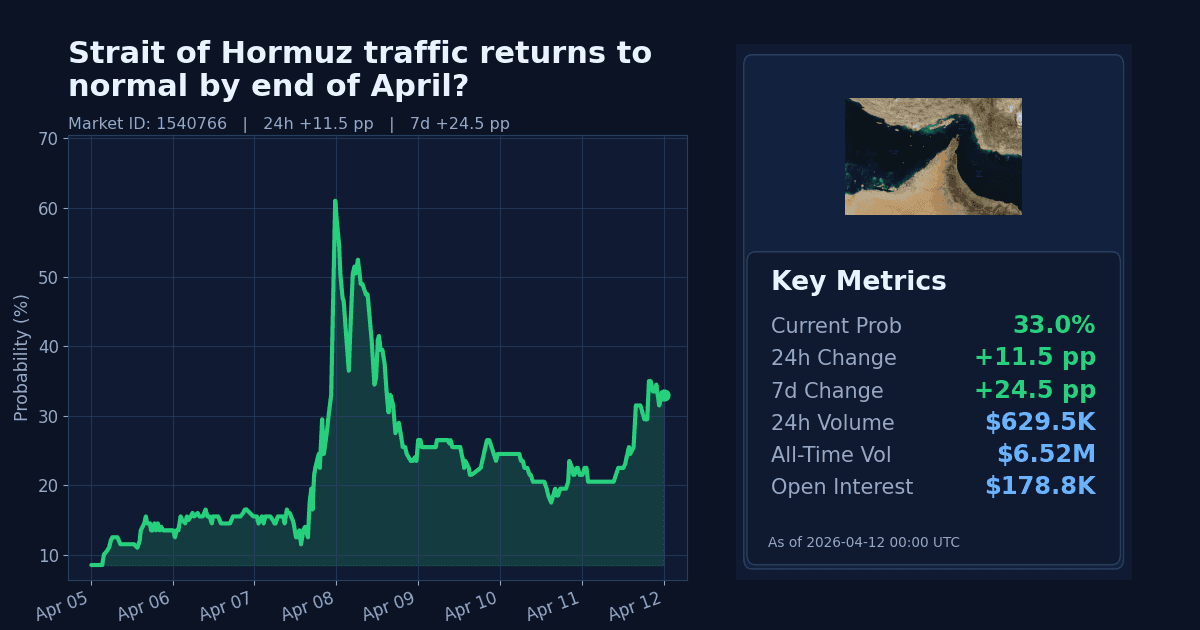

The Polymarket contract on whether IMF Portwatch will show the Strait of Hormuz’s 7‑day moving average of transit calls at or above 60 on any date between March 9 and April 30, 2026 moved sharply higher. The Yes probability increased by 11.5 percentage points over 24 hours to 33.0% as of April 12, 2026.

Over the past week, the market is up 24.5 percentage points. Trading activity is elevated, with a 24‑hour volume of $629,469.53 and open interest of $178,753.72; the quoted spread is 1.0 percentage point.

Why It Likely Moved

- The repricing appears driven by de‑escalation signals, including reports of direct U.S.–Iran talks in Pakistan while a fragile ceasefire holds, which markets may see as supportive of safer shipping conditions before April 30, 2026, according to Ground News (April 11).

- Policy coordination on energy security from EU institutions likely contributed: the European Commission convened an Oil Coordination Group on April 8 to assess the oil supply situation as Middle East disruptions entered their sixth week, and confirmed gas preparedness via the Gas Coordination Group on April 9, per official EU Commission and EU Commission statements.

- Cross‑market signals of de‑escalation reinforced the move: related markets repriced toward an end to active hostilities around Iran through late April, aligning with an improved outlook for maritime traffic normalization.

- Macro context aligns with reduced risk premia: Brent crude is $95.2/bbl and down 12.7% over 7 days, while the VIX fell 19.4% over 7 days, indicating softer energy and broader risk stress (data as of April 10).

- A counter‑signal remains: the U.S. told The New York Times that Iran lost track of mines laid in the Strait, complicating clearance and reopening, per Ground News (April 11). The latest price action suggests markets weighed broader de‑escalation and policy readiness more heavily than this operational risk.

How Strong the Move Is

The 24‑hour shift is classified as extreme by the market’s own z‑score framework (z = 48.0), indicating an unusually large single‑day repricing in the recent trading history. The 11.5pp rise to 33% is a significant intraday spike.

On a 7‑day basis, the move is sharp (z ≈ 2.31), with a cumulative 24.5pp increase. This looks like a rapid, event‑driven upswing rather than a gradual trend, and it follows de‑escalation cues within the contract window ending April 30, 2026.

Cross-Market Confirmation

- “Military action against Iran ends on April 9, 2026?” trades at 98.6% (Δ24h: +1.15pp; Δ7d: +97.75pp), confirming a strong de‑escalation signal consistent with higher odds of shipping normalization.

- “Military action against Iran continues through April 30, 2026?” is at 1.3% (Δ24h: −0.30pp; Δ7d: −76.35pp), reinforcing the view that hostilities are unlikely to persist, supportive of the main market’s move.

- “Kharg Island no longer under Iranian control by April 30?” sits at 7.0% (Δ24h: −1.0pp; Δ7d: −11.0pp), implying low perceived risk of major territorial shifts; this aligns with a stabilization narrative for Gulf shipping conditions.

News & Real-World Context

- On April 11, U.S. officials said Iran lost track of mines it laid in the Strait, complicating clearance and traffic resumption, per Ground News. The same day, U.S. warships transited the Strait for the first time since the Iran war began, signaling a shift in naval posture, according to Axios (April 11).

- Direct U.S.–Iran talks in Pakistan occurred as a fragile ceasefire held, per Ground News (April 11), adding diplomatic support to de‑escalation.

- The European Commission convened the Oil Coordination Group on April 8 to assess oil security of supply amid Middle East disruptions in their sixth week, and on April 9 the Gas Coordination Group confirmed EU gas preparedness, per official EU Commission and EU Commission releases. These are explicit policy signals on energy resilience.

- On April 10, the European Parliament published a written question on direct diplomacy with Iran to protect critical raw materials, indicating EU‑level engagement with supply‑security risks.

- On April 7, the UK government explained its UN Security Council vote on a Middle East resolution, underscoring the UK’s official stance amid the crisis.

Bottom Line

This is an extreme single‑day repricing toward a return to normal Strait traffic before April 30, likely anchored in de‑escalation signals and visible EU energy‑security coordination. However, unresolved hazards like mine clearance pose material downside to rapid normalization. The move looks like a short‑term, event‑driven shift with uncertain follow‑through.

Market Conditions at Time of Writing

- Current Probability: 33.0%

- 24h Change: +11.5pp

- 7d Change: +24.5pp

- Volume (24h): $629,469.53

- Open Interest: $178,753.72

- Spread: 1.0pp

- Z-score (24h): 48.0