What Moved the Market

-

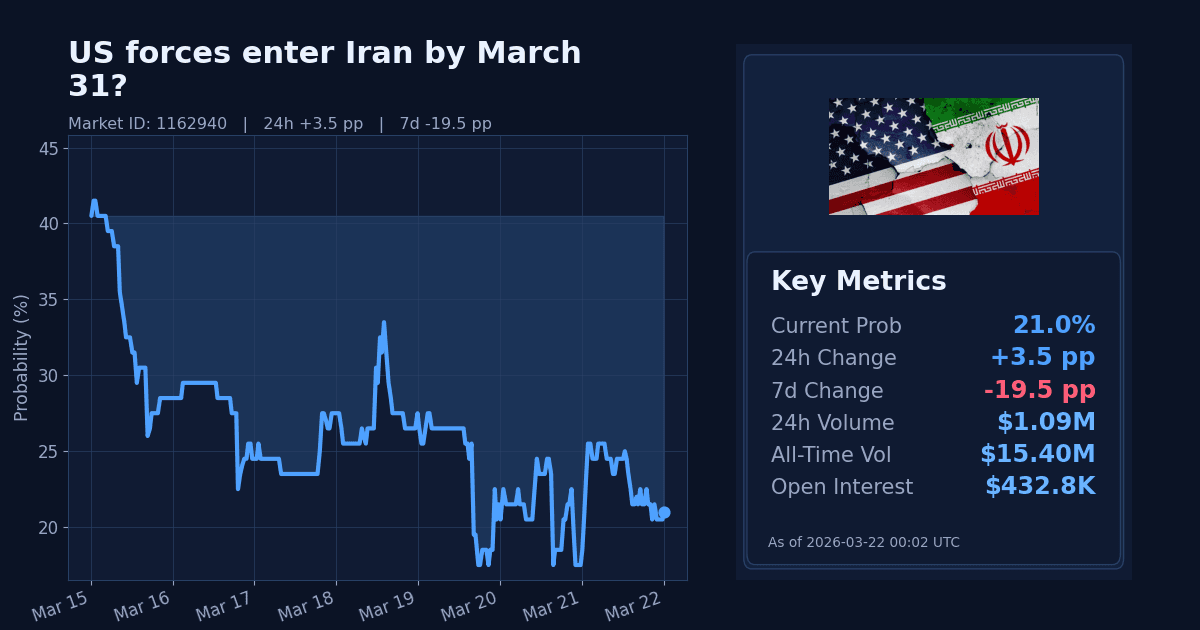

Traders are pricing the Polymarket contract on whether active U.S. military personnel will physically enter Iran by March 31, 2026 (ET). As of March 22, the market is at 21%, up 3.5 percentage points over 24 hours, while remaining down 19.5 points over the past week.

-

The late-window repricing comes with elevated 24-hour volume and a tight spread, indicating active two-way interest as the contract approaches its March 31 end date.

Why It Likely Moved

- Repricing appears driven by a fresh U.S. government update emphasizing ongoing, large-scale strikes on Iran (“devastating combat power” under Operation Epic Fury), reinforcing that operations continue rather than wind down.

- Markets reacted to news flow describing the war entering its fourth week with no clear end, which supports ongoing operational tempo and, by extension, keeps special-operations entry risk on the table.

- The move also aligns with related markets that price low odds of a near-term ceasefire or formal end to U.S. operations by March 31, reducing the perceived likelihood of imminent de-escalation.

- Energy benchmarks remain elevated, with WTI at $98.23 (+47.87% over 30 days) and Brent at $106.41 (+48.49% over 30 days, as of Mar 20), a backdrop consistent with persistent conflict risk that can sustain tail probabilities in escalation-sensitive markets.

How Strong the Move Is

-

The 24-hour shift is classified as extreme by the market’s own z-score (z=12.0), indicating the size of the daily uptick is unusual relative to recent trading history. On a pure flow basis, the jump looks like a significant short-term spike.

-

However, the 7-day change remains a normal-to-down move overall, at -19.5pp with a normal z-score profile. Taken together, this suggests a corrective rebound within a broader weekly pullback rather than a decisive trend reversal.

Cross-Market Confirmation

- “Trump announces end of military operations against Iran by March 31?” sits at 10%, consistent with limited expectation of near-term de-escalation and supportive of a modest bid in the entry-risk market.

- “US x Iran ceasefire by March 31?” at 8% also aligns with continued operations through month-end, reinforcing the main market’s upward tick.

- “US x Iran ceasefire by April 15?” at 23% signals somewhat greater odds of de-escalation beyond March, which does not contradict the current market’s late-March risk repricing.

News & Real-World Context

- Official U.S. communications highlight continuing strikes on Iran, underscoring active engagement rather than a pause. Parallel reporting notes the war has entered a fourth week without a clear endpoint.

- Additional coverage points to ongoing damage from joint U.S.-Israeli strikes, including to cultural heritage sites, emphasizing the intensity and breadth of operations.

- At the same time, statements about considering a “winding down” and steps to ease the energy crunch (including discussion of oil-related measures) introduce a de-escalatory thread in the narrative, which may limit the upside in near-term entry odds.

- Broader geopolitical maneuvering, including reports of rejected intelligence-swap overtures, reflects a complex environment but does not provide a direct signal toward imminent ground entry within the contract window.

Bottom Line

- The contract saw an extreme daily bounce, likely tied to official and media signals that active U.S. operations are continuing as the end date approaches.

- Given the market’s weekly decline and mixed de-escalation rhetoric, the move looks short-term rather than structural.

Market Conditions at Time of Writing

- Current Probability (%): 21.0

- 24h Change (pp): +3.5

- 7d Change (pp): -19.5

- Volume (24h, $): 1,087,843.75

- Open Interest ($): 432,770.85

- Spread (pp): 1.0

- Z-score (24h): 12.0