What Moved the Market

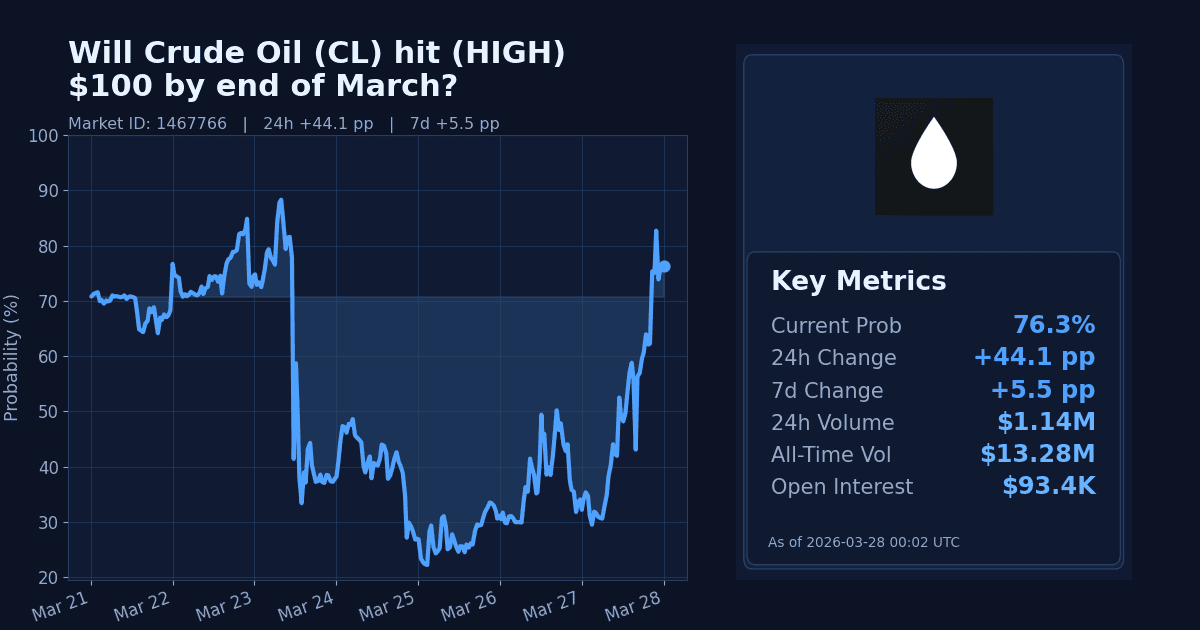

The Polymarket contract “Will Crude Oil (CL) hit (HIGH) $100 by end of March?” surged to 76.3% as of March 28, a 44.1 percentage point rise over 24 hours. The move prices the chance that, by March 31, 2026, the CME front‑month crude oil (CL) official settlement reaches at least $100.

This repricing arrives late in the contract window (market start: February 28, 2026; end: March 31, 2026), with only the active-month CME settlements through March 31 able to resolve the market.

Why It Likely Moved

- The repricing appears driven by benchmarks already above the threshold: WTI crude was $101.18 per barrel as of March 27, 2026, per Yahoo Finance, up 54.7% over 30 days and 2.9% over 7 days, reducing uncertainty about at least one ≥$100 CME settlement before March 31.

- Policy signals: on March 26, Members of the European Parliament raised formal written questions on Strait of Hormuz disruption risks to fertiliser supply (European Parliament, 2026‑03‑26) and on maritime war‑risk insurance and European energy security (European Parliament, 2026‑03‑26). These underscore official concern over shipping and energy-route risks.

- Markets reacted to sustained conflict-linked supply uncertainty: reporting describes Iran‑related disruptions to shipping and energy routes and elevated market risk (AP News, 2026‑03‑27).

- Additional context on volatility and escalation risk likely supported higher risk premia: analyses highlight war‑driven oil market uncertainty (NPR, 2026‑03‑27) and Iran’s broader escalation targeting critical infrastructure and energy assets (CSIS, 2026‑03‑27).

How Strong the Move Is

The 24‑hour shift (+44.1pp) registers as an extreme move by the market’s own history (24h z‑score: 176.4). This indicates an abrupt repricing rather than ordinary day‑to‑day noise.

Over seven days, the increase is more measured (+5.5pp) and falls within normal volatility for this market (7d z‑score: 0.53). Put differently, the latest jump is a sharp, late‑window spike atop an already firm weekly trend.

Cross-Market Confirmation

- “Will Crude Oil (CL) hit (HIGH) $95 by end of March?” trades at 99.9%, consistent with the $100 market’s upswing. 24h/7d deltas unavailable; level strongly confirms proximity to higher thresholds.

- “US x Iran ceasefire by March 31?” is at 3.8%, signaling low near‑term de‑escalation expectations; this aligns with a persistent risk premium into March-end. Deltas unavailable.

- “US x Iran ceasefire by April 30?” at 40.0% implies higher de‑escalation odds beyond March, a partial divergence that confines highest risk premia to the immediate window. Deltas unavailable.

News & Real-World Context

- On March 27, AP reported Iran’s insurgent-style tactics have disrupted shipping and energy routes, heightening market risks and volatility (AP News, 2026‑03‑27).

- NPR on March 27 emphasized that uncertainty over the Iran war’s duration is generating unusual, sometimes contradictory moves and elevated oil volatility (NPR, 2026‑03‑27). A companion piece surveyed regional spillovers, including tensions near energy chokepoints (NPR, 2026‑03‑27).

- CSIS on March 27 detailed Iran’s escalation, including threats to critical infrastructure and energy facilities, as a driver of market disruption risk (CSIS, 2026‑03‑27).

- As official policy signals, the European Parliament’s March 26 written questions flagged Hormuz-linked supply risks (European Parliament, 2026‑03‑26) and maritime war‑risk insurance implications for European energy security (European Parliament, 2026‑03‑26).

- Macro backdrop corroborates stress: the VIX stands at 31.05, up 15.9% over 7 days and 73.2% over 30 days, consistent with heightened cross‑asset risk premia.

Bottom Line

The market rapidly repriced toward “Yes” as benchmark crude traded above $100 and official EU and analytical sources highlighted elevated disruption risks around Iran and the Strait of Hormuz. With resolution tied to any qualifying CME settlement by March 31, this looks like a late‑window, event‑driven spike rather than a structural shift.

Market Conditions at Time of Writing

- Current Probability: 76.3%

- 24h Change: +44.1pp

- 7d Change: +5.5pp

- Volume (24h, $): 1,135,927.99

- Open Interest ($): 93,436.46

- Spread (pp): 2.9

- Z-score (24h): 176.4