What Moved the Market

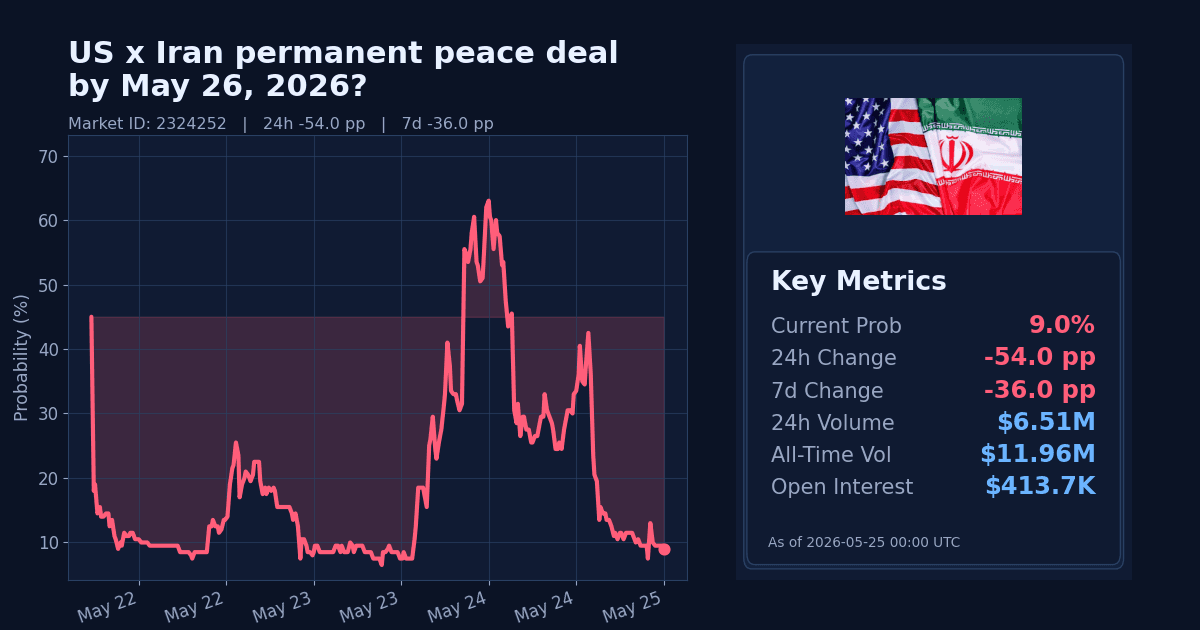

The Polymarket contract on a “US × Iran permanent peace deal by May 26, 2026” sharply repriced lower, dropping 54 percentage points in the last 24 hours to 9%. The move comes with the market set to end on May 26, 2026 at 11:59 PM ET, after opening on May 21, 2026.

Over the past week the contract is down 36 percentage points. Trading was heavy into the selloff, with $6.51M in 24h volume and a 1.0 pp spread at the time of writing.

Why It Likely Moved

- The deadline is imminent and the market’s criteria require a written agreement or clear dual government confirmation explicitly ending military hostilities on a lasting basis; temporary ceasefires do not qualify under the market rules.

- Reporting on May 24 points to proposals focused on a ceasefire and de-escalation around the Strait of Hormuz, rather than a permanent peace agreement, according to AP News.

- Domestic political pushback in the US was reported the same day, with Republican critics panning the emerging proposal, suggesting headwinds to rapid formalization of any deal language, per AP News (May 24).

- Europe’s posture appears punitive rather than conciliatory: the EU is reportedly moving toward sanctions on Iran over a Hormuz blockade, according to a Reuters-based brief via Ground News (May 24), which is not consistent with an imminent permanent peace announcement.

- No official US or Iranian government confirmation of a permanent peace deal appears in the supplied government materials; the most relevant US item is a May 22 White House OSTP post of remarks on nuclear executive orders, which does not announce any US–Iran peace accord (White House OSTP, May 22).

How Strong the Move Is

The 24-hour drop registers an extreme z-score of 212, indicating an unusually sharp one-day repricing relative to this market’s recent trading history. By contrast, the seven-day z-score is labeled normal, suggesting the magnitude of the weekly change is in line with prior volatility.

Taken together, this looks like an extreme, deadline-driven downside spike rather than a multi-week trend shift.

Cross-Market Confirmation

- A near-identical market expiring May 31 fell 46.5 pp over 24h to 24%, while rising 16 pp over 7d — confirming short-term pessimism but showing higher confidence for a later window.

- The June 30 variant dropped 31.5 pp in 24h to 46%, yet is up 21 pp over 7d — a directional 24h confirmation with 7d divergence (more optimism later).

- The July 31 contract declined 17.5 pp in 24h to 62%, and is up 29 pp on the week — the smallest 24h drop and the largest 7d gain, reinforcing the pattern: near-term odds were marked down far more than medium-term odds.

News & Real-World Context

- On May 24, AP reported details of a possible US–Iran arrangement centering on a ceasefire and steps to reduce hostilities around the Strait of Hormuz, following an announcement of “progress” by President Trump. Crucially, the reporting describes de-escalation measures, not a definitive, permanent end to hostilities (AP News, May 24).

- Also on May 24, AP noted Republican criticism of the emerging proposal, underscoring domestic divisions that could slow or dilute any agreement language (AP News).

- European pressure appears to be increasing: Reuters reporting summarized by Ground News said the EU is moving to sanction Iran over a Hormuz blockade (Ground News, May 24).

- In official US communications, the White House Office of Science and Technology Policy published remarks on May 22 marking the one-year anniversary of nuclear executive orders, without any reference to a US–Iran permanent peace announcement (White House OSTP, May 22).

Macro indicators offer limited confirmation of a discrete peace breakthrough: Brent crude is $100.21/bbl and down 8.28% over 7 days, while the VIX fell 9.39% over the week and the US Dollar Index slipped 0.27%. These broader moves suggest easing market stress, but they do not provide direct evidence of an imminent, permanent US–Iran peace deal.

Bottom Line

The sharp selloff appears to reflect the high bar set by this market’s rules and the imminent May 26 deadline, alongside reporting that emphasizes ceasefire de-escalation rather than a lasting end to hostilities, plus evident political resistance. Related markets confirm a near-term markdown but retain higher odds for later expiries.

This looks like a short-term, deadline-driven repricing rather than a structural shift in expectations about a permanent peace this summer.

Market Conditions at Time of Writing

- Current Probability: 9%

- 24h Change: -54 pp

- 7d Change: -36 pp

- Volume (24h, $): 6,513,028.59

- Open Interest ($): 413,677.15

- Spread (pp): 1.0

- Z-score (24h): 212.0