What Moved the Market

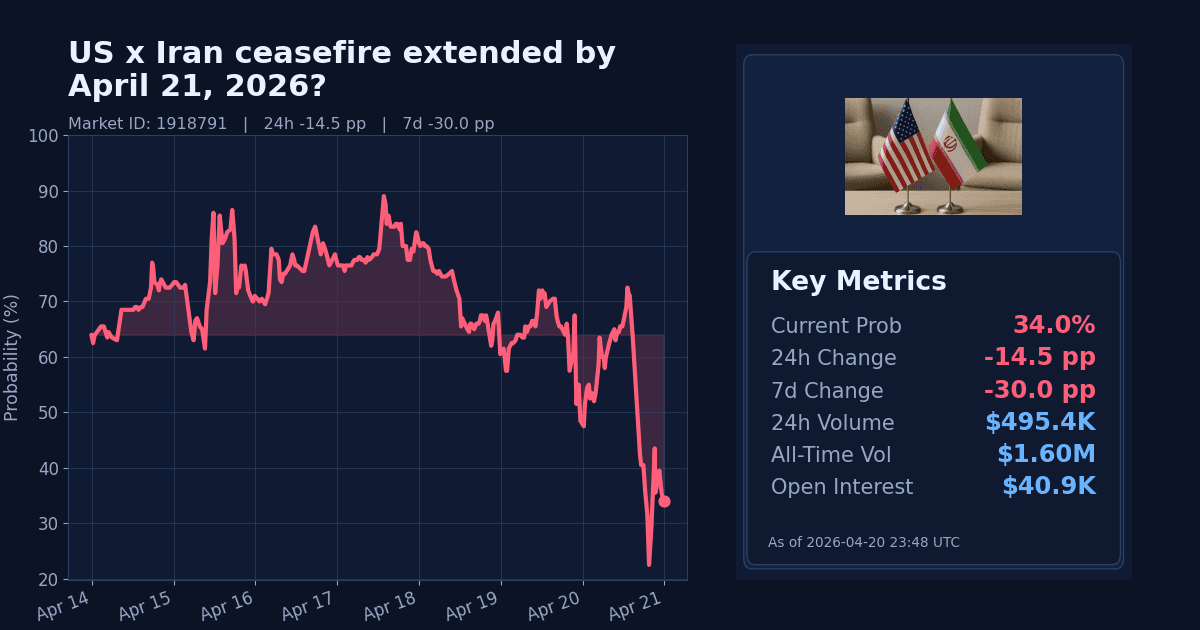

The Polymarket contract “US x Iran ceasefire extended by April 21, 2026?” tracks whether Washington and Tehran will officially extend the two‑week halt in direct hostilities announced on April 7, 2026, by 11:59 PM ET on April 21, 2026. As of April 20, 2026 (23:48 UTC), the market price implies a 34% probability of an extension.

Over the past 24 hours, the contract fell 14.5 percentage points. Over the past week, it is down 30 points. The sharp decline arrives inside the market window (Apr 8–21) as the initial ceasefire period nears expiry.

Why It Likely Moved

- The repricing appears driven by official US action: on April 20, the US government stated that its forces disabled an Iranian‑flagged cargo vessel attempting to violate a blockade, signaling escalatory enforcement during the ceasefire window (U.S. government, 2026‑04‑20).

- Markets reacted to reporting that peace talks were thrown into doubt after the United States seized an Iranian ship, with Tehran expressing reluctance to proceed; President Trump said a US delegation would travel to Pakistan to resume talks (NPR, 2026‑04‑20).

- The move also aligns with allied caution that a rushed framework could backfire if technical details remain unresolved, implying limited scope for a fast, clean extension before the deadline (Ground News, 2026‑04‑20).

- Additional context notes a two‑week US–Iran ceasefire nearing its end alongside other regional negotiations, underscoring a compressed timeline for a formal, mutually confirmed extension (NPR, 2026‑04‑20).

How Strong the Move Is

The 24‑hour decline is classified as extreme by the market’s own z‑score metric, indicating the drop is unusually large versus recent trading patterns. The single‑day move stands out rather than blending into normal volatility.

The 7‑day change is also labeled extreme to the downside, suggesting a multi‑session deterioration in odds rather than a one‑off headline shock. Together, these point to a sharp, deadline‑proximate drawdown rather than noise.

Cross-Market Confirmation

- US x Iran permanent peace deal by April 22, 2026: 12% (−4pp 24h). This confirms weaker near‑term de‑escalation expectations.

- US x Iran permanent peace deal by April 30, 2026: 35% (+13pp 7d). This diverges somewhat, indicating some market belief in a later breakthrough beyond the ceasefire‑extension deadline.

- US x Iran diplomatic meeting by April 22, 2026: 70% (+4pp 24h, −1.5pp 7d). This diverges: participants price talks as likely while marking down the odds of an immediate, formal extension.

- Macro backdrop: Brent crude is $94.91/bbl, down 4.5% over 7 days and 15.4% over 30 days, while the VIX is 18.87 and down 1.3% over 7 days. Energy and volatility benchmarks do not show concurrent stress spikes, offering no cross‑asset confirmation of an acute, market‑wide escalation (Brent, VIX as of 2026‑04‑20).

News & Real-World Context

- The most direct policy signal came on April 20 from the U.S. government, which announced its forces disabled an Iranian‑flagged cargo vessel attempting to enter an Iranian port in violation of blockade measures (U.S. government, 2026‑04‑20).

- The same day, reporting indicated the U.S. seizure of an Iranian ship complicated prospects for talks; President Trump said a delegation would travel to Pakistan to resume negotiations, but Tehran signaled reluctance (NPR, 2026‑04‑20).

- European allies warned that rushing a US–Iran framework could backfire by locking in technical deadlocks that are difficult to implement, which could hinder quick agreement on an extension (Ground News, 2026‑04‑20).

- Separately, EU policymakers flagged downstream impacts of Middle East conflict on fuel prices in a written question to the Commission, underscoring ongoing regional risk considerations within official EU channels (European Parliament, 2026‑04‑20).

Bottom Line

Pricing for a ceasefire extension by the April 21 deadline has fallen sharply following an official US blockade enforcement action and reporting that ship seizure has complicated near‑term talks. Related markets suggest diplomacy remains possible, but immediate, formal extension confirmation from both governments now looks less likely on this timeline.

Market Conditions at Time of Writing

- Current Probability: 34%

- 24h Change: −14.5pp

- 7d Change: −30pp

- Volume (24h, $): 495,432.76

- Open Interest ($): 40,949.23

- Spread (pp): 2.0

- Z-score (24h): 52.0