What Moved the Market

-

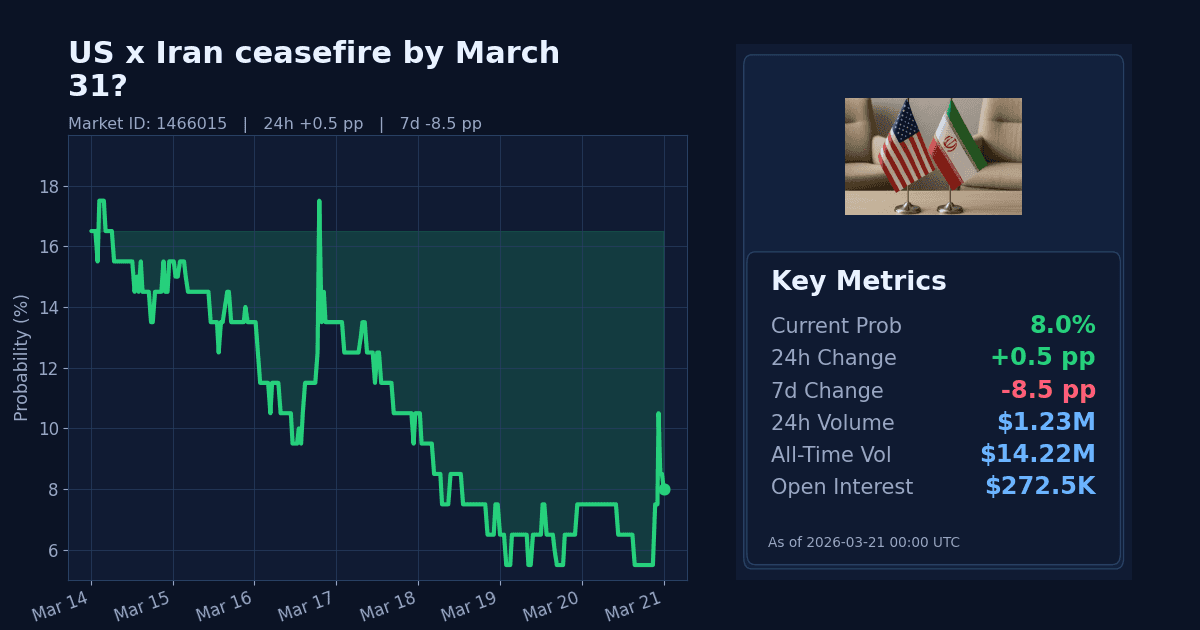

The market on an official, publicly confirmed ceasefire between the United States and Iran by March 31 (11:59 PM ET) is priced at 8% as of March 21. Over the past week, it declined by 8.5 percentage points, with a modest 0.5 pp uptick over the last 24 hours.

-

Launched on February 28, 2026, the contract covers a mutually announced halt in hostilities by both governments. Recent trading shows a weekly slide and largely flat day-to-day movement into the final stretch of the contract window.

Why It Likely Moved

- Repricing appears driven by the approaching March 31 deadline without corresponding official statements from Washington or Tehran indicating a negotiated halt.

- Markets reacted to ongoing conflict signals, including reports of continued strikes and additional US Marines and warships heading toward the region, which reduce the plausibility of a near-term bilateral ceasefire.

- The slowdown or halting of shipping through the Strait of Hormuz and allied moves to secure the waterway suggest persistent tensions rather than imminent de-escalation, informing lower odds within the current window.

- Elevated energy benchmarks—Brent crude near $106.77 and up roughly 52% over 30 days—appear consistent with continued geopolitical risk, reinforcing market skepticism about a rapid ceasefire.

How Strong the Move Is

-

The 24-hour move is small (+0.5 pp) and the platform’s 24h z-score characterization is “normal,” indicating no unusual volatility in the latest session. The 7-day change (−8.5 pp) also carries a “normal” z-score label relative to recent volatility.

-

Taken together, this looks like a steady, deadline-driven repricing rather than a sharp dislocation. With the contract window closing in under two weeks, the decline reads as a continuation of a short-term trend toward lower odds absent new, official ceasefire signals.

Cross-Market Confirmation

- A related market on a US–Iran ceasefire by April 15 is priced higher (24%), which aligns with the idea that traders see more time as necessary; this confirms the bearishness specific to a March 31 deadline.

- Markets on potential US forces entering Iran show 18% by March 31 and 53% by April 30, implying elevated expectations of confrontation in the near term and medium term; this stance is directionally consistent with lower ceasefire odds for March.

- Higher pricing in escalation-focused contracts, alongside relatively low March ceasefire odds, collectively points to a risk skew toward continued tension rather than a rapid bilateral halt in hostilities.

News & Real-World Context

-

Recent reporting describes an ongoing “Iran war,” further strikes involving Iran, and US force movements toward the Middle East. European nations, Japan, and Canada signaled support for efforts to secure the Strait of Hormuz as shipping through the strait has been severely disrupted.

-

The disruptions carry broader economic implications: the WTO flagged downside risks to world trade growth tied to the conflict, and energy markets remain elevated. Brent crude is around $106.77 and WTI near $98, each up roughly 50% over the month, underscoring persistent geopolitical supply risk that is not typically associated with imminent ceasefires.

Bottom Line

- The March 31 US–Iran ceasefire contract has drifted lower to 8% over the past week and remains subdued. Traders appear to be pricing the combination of a closing window, continuing hostilities, and lack of formal diplomatic signals.

- The move looks short-term and deadline-driven rather than structural. Without clear, public confirmation from both governments, the market is unlikely to re-rate meaningfully higher.

Market Conditions at Time of Writing

- Current Probability (%): 8.0

- 24h Change (pp): +0.5

- 7d Change (pp): -8.5

- Volume (24h, $): 1,233,828.34

- Open Interest ($): 272,496.81

- Spread (pp): 1.0

- Z-score (24h): 0.0