What Moved the Market

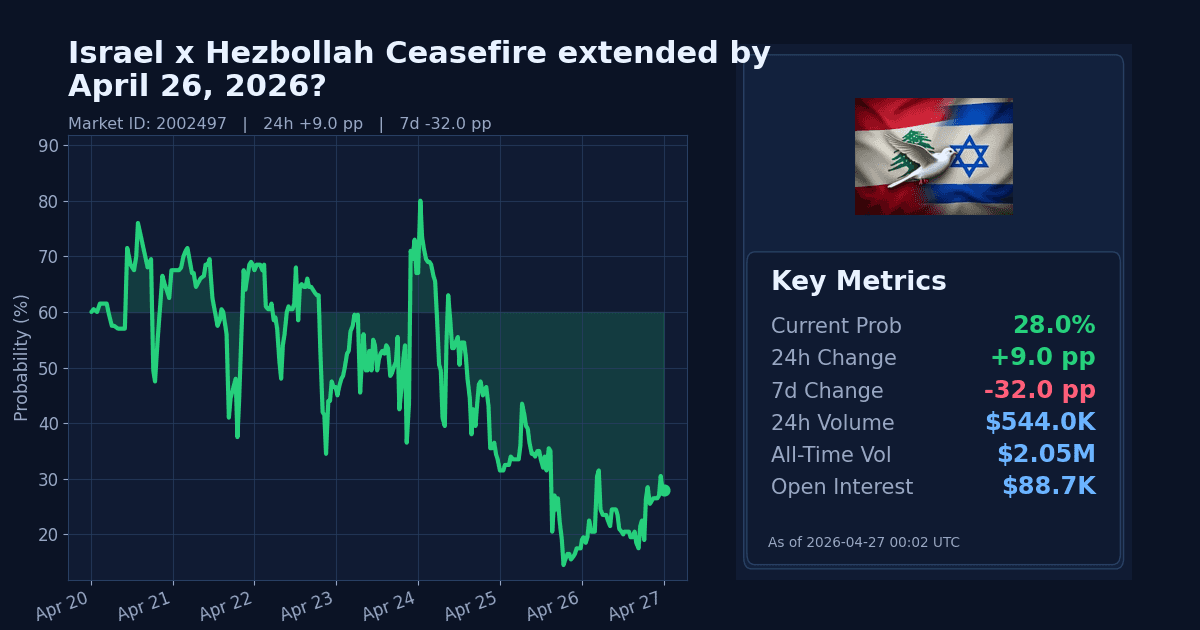

The Polymarket contract asks whether the 10‑day Israel–Hezbollah ceasefire announced on April 16, 2026 will be officially extended by April 26, 2026 at 11:59 PM ET. As of publication time, the market price implies a 28% probability.

Over the past 24 hours, the probability climbed 9 percentage points to 28%. Over the past seven days, it fell 32 percentage points, marking a pronounced weekly decline despite the late rebound.

Why It Likely Moved

- The late 24h rebound appears driven by repricing as the April 26 resolution window closes, with traders adjusting positions into the contract deadline.

- The week‑on‑week selloff aligns with related de‑escalation markets turning lower, suggesting diminished expectations for rapid regional diplomacy.

- Energy risk proxies moved higher this week: Brent crude is at $101.31 per barrel, up about 12% over 7 days, reinforcing a risk premium consistent with reduced confidence in sustained calm.

- Israeli domestic political signals on April 26 — including mounting public dissatisfaction with the government’s security outcomes and opposition coordination — added uncertainty that markets may have factored into near‑term negotiating bandwidth, according to AP News and AP News.

- Official policy attention remained elevated: the European Parliament (Apr 24) raised risks of aviation fuel shortages due to the Middle East war, while separate EP questions (Apr 22) addressed Israel’s compliance with the EU‑Israel Association Agreement (item 1; item 2). The UK government and UAE issued a joint statement on April 25, underscoring active diplomatic engagement.

How Strong the Move Is

The 24‑hour upswing is classified as sharp relative to recent trading (z‑score 2.53), indicating a notable late move into the event window. By contrast, the seven‑day decline is extreme (z‑score 9.87), pointing to a decisive weekly repricing lower.

Taken together, this looks like a sharp daily bounce within an extreme weekly selloff, rather than a full reversal of the broader move.

Cross-Market Confirmation

- US × Iran permanent peace deal by Apr 30, 2026: −2.05pp (24h), −32.45pp (7d). Confirms the weekly deterioration in de‑escalation odds; diverges from today’s uptick in the ceasefire‑extension market.

- US × Iran permanent peace deal by May 31, 2026: −1.0pp (24h), −22.5pp (7d). Also confirms weaker weekly de‑escalation sentiment; 24h move modestly diverges.

- US × Iran permanent peace deal by Jun 30, 2026: +4.0pp (24h), −15.0pp (7d). Mixed: modest 24h support but still weaker on the week.

Overall, related markets align with the weekly drop in extension odds, while offering no consistent confirmation of the 24h bounce.

News & Real-World Context

- Israeli political dynamics intensified on April 26: Prime Minister Netanyahu’s government faces public dissatisfaction over unmet objectives against Iran and rising election pressures, per AP News. Separately, two former prime ministers agreed to merge parties to challenge Netanyahu, adding to political flux, according to AP News.

- Regional diplomacy faced headwinds on April 26 as talks in Pakistan were put on hold after Iran’s top diplomat left Islamabad and envoys for Donald Trump did not attend, stalling ceasefire‑oriented discussions, reported AP News.

- Government signals: The UK government and UAE issued a joint statement on April 25. The European Parliament (Apr 24) queried aviation fuel shortage risks from the Middle East war and raised scrutiny of EU–Israel relations via written questions on Apr 22 (compliance review; possible suspension).

- Macro backdrop: Brent crude at $101.31 is up ~12% over 7 days, while the VIX rose ~7% over the week, indicating a firmer risk premium alongside energy‑market sensitivity to Middle East developments.

Bottom Line

The market staged a sharp late bounce into the deadline but remains materially lower on the week, consistent with softer regional de‑escalation signals and a firmer energy‑risk tone. Cross‑markets and policy scrutiny support the weekly downdraft; near‑term pricing still reflects deadline‑driven uncertainty.

Market Conditions at Time of Writing

- Current Probability: 28%

- 24h Change: +9pp

- 7d Change: −32pp

- Volume (24h): $543,989.61

- Open Interest: $88,689.96

- Spread: 2.0pp

- Z‑score (24h): 2.53 (sharp)