What Moved the Market

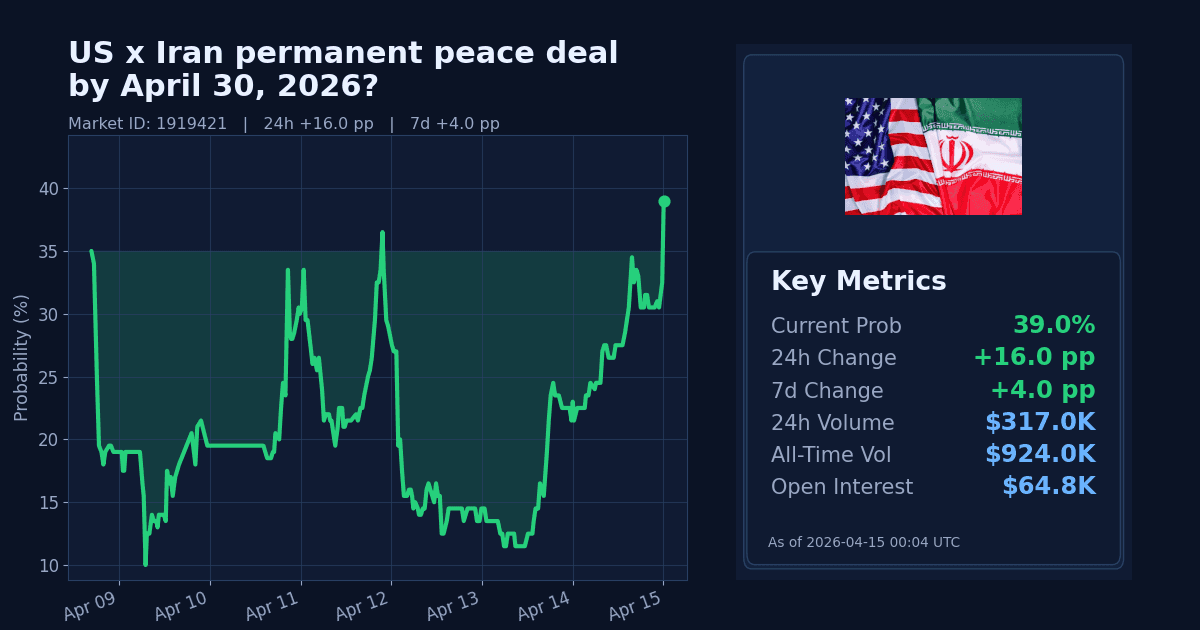

The Polymarket contract on a “permanent peace deal” between the United States and Iran by April 30, 2026 moved sharply higher, with the implied probability rising to 39% as of April 15.

This repricing occurred within a narrow contract window (market runs April 8–30, 2026), signaling a fast reassessment of near-term diplomatic outcomes.

Why It Likely Moved

- The repricing appears driven by headlines indicating a potential return of US and Iranian teams to Islamabad for renewed talks this week, per Reuters (via Ground News) on April 14.

- Markets also reacted to reports of preparations for a second round of talks despite ongoing tensions, according to AP News on April 14.

- Risk sentiment and energy pricing shifted alongside these headlines: global shares gained and oil fell on talk-renewal hopes, per AP News on April 14.

- Macro context is consistent with de-escalation pricing: Brent crude stands at $93.6/bbl and is down 14.3% over 7 days, while the VIX is 18.36, down 28.8% over 7 days, as of April 14.

How Strong the Move Is

The 24-hour move registers as extreme by this market’s standards (24h z-score 64.0), indicating an outsized, headline-driven jump rather than routine drift. By contrast, the 7-day z-score is normal (0.0).

On a weekly basis, the contract is only modestly higher (+4pp over 7 days), suggesting the latest spike is recent and concentrated rather than a long-building trend.

Cross-Market Confirmation

- US–Iran permanent peace deal by April 22, 2026: up 6pp over 24h to 20% — directional alignment with the main market’s move.

- Israel–Hezbollah ceasefire by April 15, 2026: down 4.95pp over 24h to 6.2% — a divergence, implying broader regional ceasefire expectations did not improve in tandem.

- Military action against Iran ends by April 17, 2026: +51.95pp over 7 days to 99.9% — strong weekly alignment with de-escalation expectations, though no notable 24h change.

News & Real-World Context

- Diplomatic track: Reports that US and Iranian teams could return to Islamabad this week for renewed talks supported de-escalation hopes (Reuters via Ground News, April 14). Separate coverage noted preparations for a second round of talks even as frictions continued in the Strait of Hormuz (AP News, April 14).

- Market reaction: Global equities firmed and oil eased on the talk-renewal reports (AP News, April 14).

- Official signals: The European Parliament (written question E‑001403/2026, April 14) highlighted EU energy security and inflation risks tied to Strait of Hormuz tensions, underscoring policy attention to de-escalation outcomes. On April 13, the European Commission President addressed the economic impact of the Middle East crisis on the EU. The UK government issued a joint foreign ministers’ statement on Lebanon on April 14, reflecting broader official focus on regional stability.

- Macro backdrop: The IMF warned of weaker global growth and higher inflation due to fallout from the Iran conflict (AP News, April 14) and flagged substantial euro‑area growth risks even if a war involving Iran is quickly resolved (Ground News, April 14).

Bottom Line

Odds jumped on concentrated, late-window headlines about potential US–Iran talks resuming and a concurrent easing in energy and volatility benchmarks. With the contract expiring April 30, 2026 and no official bilateral confirmation of a permanent peace agreement, the move looks headline-driven rather than structural.

A durable re-rating likely depends on definitive, public confirmation from both governments or a signed text meeting the market’s criteria.

Market Conditions at Time of Writing

- Current Probability: 39%

- 24h Change: +16pp

- 7d Change: +4pp

- Volume (24h, $): 317,044.94

- Open Interest ($): 64,765.83

- Spread (pp): 2.0

- Z-score (24h): 64.0