What Moved the Market

-

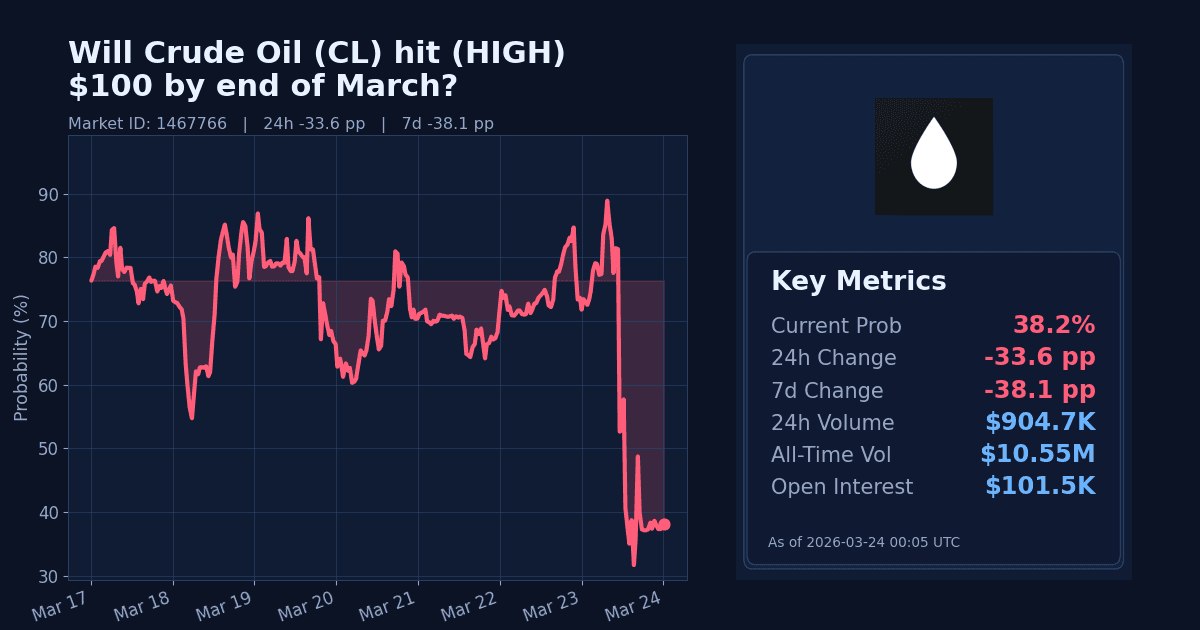

This market asks whether the CME Active Month Crude Oil (CL) futures settlement will reach or exceed $100 on any trading day by the final trading day of March 2026. As of March 24, pricing for a “Yes” outcome moved sharply lower to around 38%.

-

The reprice occurred late in the contract window (market start: Feb 28, 2026; end: Mar 31, 2026), with only a few trading days remaining for a qualifying $100 settlement.

Why It Likely Moved

- Markets reacted to headlines suggesting a potential diplomatic opening between the U.S. and Iran, including an extended deadline related to the Strait of Hormuz, which appears to have eased immediate supply-risk fears.

- Repricing follows softer spot benchmarks: WTI near $89.5/bbl and Brent close to $101/bbl, levels that reduce the near-term probability of a $100 CME CL settlement before month-end.

- News flow indicating oil “eased” alongside a broader risk-on equity move appears driven by comments that talks may be occurring, even as Iranian officials denied negotiations, tempering acute tail-risk.

- The shift also aligns with recent guidance that markets have been volatile amid the Middle East conflict, and the latest move looks like an unwind of some risk premium rather than a new shock.

How Strong the Move Is

-

The 24-hour decline of 33.6 percentage points registers as statistically extreme for this market’s recent history (24h z-score: extreme down). That points to a sharp repricing rather than routine noise.

-

Over seven days, pricing is lower by 38.15pp, but the weekly z-score is characterized as normal/flat, suggesting that while levels are meaningfully down on the week, the volatility profile over that horizon remains within recent norms.

Cross-Market Confirmation

- A closely related market on CL hitting a $90 low by end of March trades near 99.7%, reinforcing the bearish tilt and lower likelihood of a $100 settlement in the remaining days.

- A separate market on a U.S.–Iran ceasefire by March 31 is around 17%, indicating no strong consensus for a formal ceasefire; this partially diverges from the de-escalation tone but is consistent with reduced, not eliminated, risk premium.

News & Real-World Context

-

Headlines point to shifting tone in the U.S.–Iran conflict: the U.S. extended a deadline tied to reopening the Strait of Hormuz and signaled openness to talks. Reports also note an easing of some sanctions on Iranian oil already at sea, moves that coincided with oil prices softening and equities rallying.

-

Earlier escalatory rhetoric around potential strikes and threats to close the Strait of Hormuz kept risk premia elevated; the subsequent tempering of immediate timelines and hints of diplomacy contributed to a pullback in crude. At one point, Brent slipped below $100 in reaction to these developments before recovering near that level.

-

Macro context: WTI sits around $89.48/bbl (down ~4.3% over 7 days but up ~34.8% over 30 days), while Brent is about $100.84/bbl. This leaves less time and distance for the CME Active Month CL settlement to print $100 before March 31.

Bottom Line

-

The probability that CL settles at or above $100 by March 31 fell sharply, consistent with de-escalation headlines and spot prices lingering well below the threshold. The move looks like a headline-driven, short-term repricing.

-

With only days left in the contract window and ongoing geopolitical uncertainty, the path to a qualifying $100 settlement remains possible but now priced as a minority outcome.

Market Conditions at Time of Writing

- Current Probability (%): 38.2

- 24h Change (pp): -33.6

- 7d Change (pp): -38.15

- Volume (24h, $): 904,668.22

- Open Interest ($): 101,496.86

- Spread (pp): 0.5

- Z-score (24h): extreme down