What Moved the Market

-

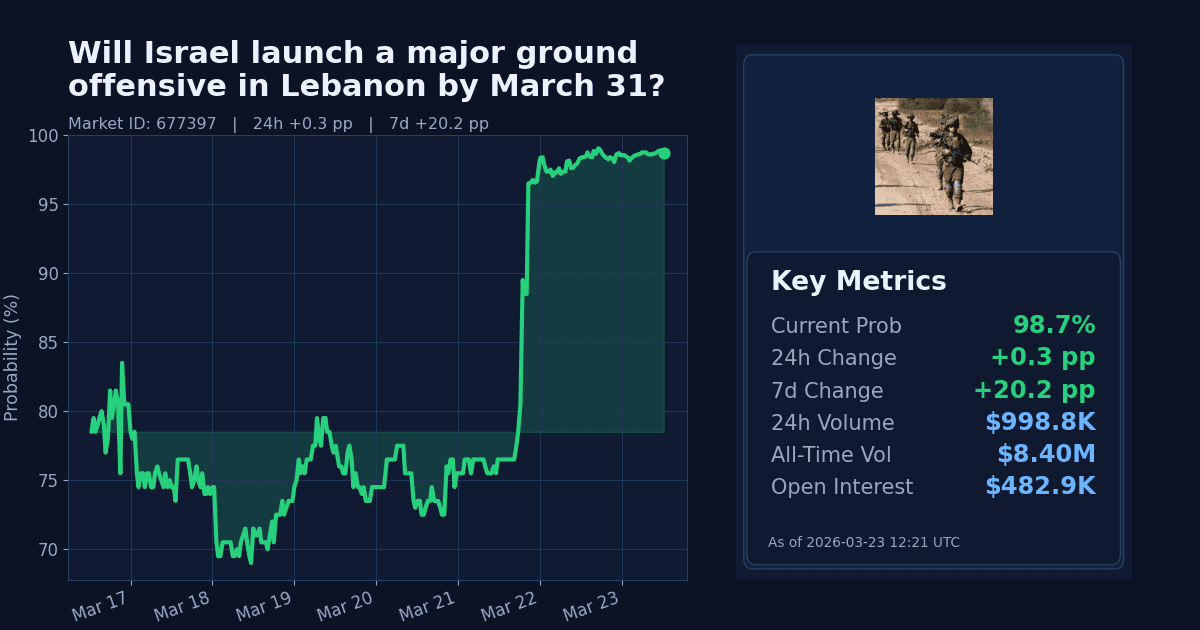

This market asks whether Israel will launch a major ground offensive in Lebanon by March 31, 2026, 11:59PM ET, defined as more than 1,000 Israeli ground forces entering Lebanese territory not under Israeli control at the start of the offensive. Over the past week, pricing moved decisively toward “Yes.”

-

As of March 23, the contract trades at 98.7%, up 20.2 percentage points over seven days and 0.3 points over the past 24 hours. Trading conditions show a tight spread and active participation into the contract’s final days.

Why It Likely Moved

- Repricing appears driven by the market entering the final stretch of the contract window, pushing traders to converge on a near-certain outcome ahead of the March 31 deadline.

- Markets reacted to broader regional escalation signals, including fresh threats and infrastructure risks that raise the perceived likelihood of expanded conflict dynamics.

- Repricing follows concurrent energy-market stress—Brent near $101/bbl and WTI above $92/bbl with strong 30-day gains—consistent with supply-risk narratives tied to regional instability.

- Strong recent buying interest, reflected in nearly $1.0M of 24h volume and a 0.1pp spread, appears to have reinforced the move toward near-certainty.

How Strong the Move Is

-

Statistical flags classify both the 24-hour and 7-day changes as extreme relative to this market’s recent trading history. This indicates the shift is not typical noise.

-

The pattern looks like a sharp late-window repricing toward resolution rather than a gradual trend, consistent with contracts approaching expiry and concentrating on binary outcomes.

Cross-Market Confirmation

- “Netanyahu out by March 31?” trades near 1.2%, suggesting leadership continuity through the same deadline; this neither confirms nor contradicts the main market’s surge.

- “Will the Iranian regime fall by March 31?” at roughly 1.4% indicates low odds of immediate regime upheaval, a neutral-to-divergent signal relative to the elevated offensive pricing.

- “Will the Iranian regime fall by June 30?” at about 23.0% implies elevated medium-term regional risk, loosely consistent with sustained tension narratives but not a direct confirmation.

News & Real-World Context

-

Recent reports highlight intensified regional risk signals. Iran warned it could strike power plants across the Gulf following a stated ultimatum on the Strait of Hormuz, pointing to potential broadening of conflict arenas.

-

The IEA chief’s assessment that more than 40 Middle East energy assets have been severely damaged underscores the scale of infrastructure disruptions and the escalation impulse priced across risk assets.

-

In parallel, energy benchmarks reflect this tension: Brent crude is around $101/bbl (up roughly 41% over the past month), while WTI is near $92/bbl (up about 39% over the month). These moves align with supply-risk narratives that often accompany heightened geopolitical strain in the region.

Bottom Line

- The market has moved to near-certainty for a “Yes” outcome by March 31, 2026, with extreme 7-day re-pricing consistent with end-of-window dynamics and regional escalation signals.

- Given the timing and breadth of risk cues, the move appears short-term and deadline-driven rather than a new structural trend.

Market Conditions at Time of Writing

- Current Probability (%): 98.7

- 24h Change (pp): +0.3

- 7d Change (pp): +20.2

- Volume (24h, $): 998,794.37

- Open Interest ($): 482,924.23

- Spread (pp): 0.1

- Z-score (24h): 6.0

- Z-score (7d): 20.0